Nigeria Payments System Vision 2028: Roadmap to a $1 Trillion Digital Economy or Another Missed Opportunity?

An in-depth analysis of Nigeria Payments System Vision 2028, examining its potential to drive a $1 trillion digital economy through innovation, financial inclusion, digital payments, fintech growth, and economic transformation.

Dr. Ohio O. Ojeagbase

Abstract

Backed by rapid growth, Nigeria’s payment landscape now ranks among Africa’s most dynamic. Looking ahead to change, the Central Bank rolled out the Nigeria Payments System Vision 2028. Not just about speed, it pushes stronger financial links alongside wider reach for excluded groups. Safety gets strong attention in this blueprint. Because digital risks are growing, efforts will stiffen safeguards across payment channels. Trust becomes more possible when systems resist attacks better. Leadership in West African digital finance becomes more achievable through coordinated improvements.

This piece dives into why PSV 2028 matters economically, weighing chances alongside hurdles built into the design, then judging potential effects across finance access, enterprise expansion, overseas capital, repayment systems, safety in transactions, and broader national progress. Based on the complete PSV 2028 blueprint, international standards, and how past programs unfolded in Nigeria, findings show the country has enough people, a vibrant fintech scene, rising digital use, and active regulation - ingredients to lead Africa in digital payments. Yet outcomes hinge on follow-through rigor, strength against cyber threats, quality of oversight, and cooperation amongst industry players. Whether it becomes a landmark shift or just another bold idea stuck in delivery only time will tell.

Keywords: Digital Payments, Financial Inclusion, Fintech, Cybersecurity, Economic Growth, Financial Security, Payment Systems, Nigeria, CBN, Digital Economy, PSV 2028.

Introduction

Nigeria's payment ecosystem has emerged as one of the fastest-growing digital payment markets in Africa. The launch of the Nigeria Payments System Vision 2028 (PSV 2028) by the Central Bank of Nigeria represents a strategic effort to modernize financial infrastructure, deepen financial inclusion, strengthen cybersecurity, and position Nigeria as not just a regional leader but continental leader in digital finance.

Back then, most people had little access to financial services. By 2030, transactions shifted massively online instead. Progress wasn’t slow - it redefined how money moves across households and markets alike. Now, trillions change hands digitally every year. One key driver? A steady push toward inclusion by regulators who saw potential early. Change didn't creep in; it arrived through policy clarity and tech upgrades together. Today's activity levels were unimaginable just fifteen years prior. Growth came not from isolated efforts but linked advancements in mobile networks, banking rules, and identity systems. Momentum built quietly at first, now shapes national spending patterns deeply.

Launched under CBN Governor Mr. Olayemi Cardoso, the Nigeria Payments System Vision 2028 (PSV 2028) aims to build on existing progress. Progress unfolds across five focused pillars meant to deepen impact. Each pillar supports advancement, though distinct in role. Together, they form a framework shaped by direction rather than force. Movement forward relies less on speed, more on alignment. Goals emerge clearly when structure follows purpose. This plan does not begin from zero, it extends what already works

1. Infrastructure and Interoperability

2. Digital Finance Access and Learning with Safeguards

3. Innovation Digital Assets Emerging Technologies

4. Cross Border Payments Meet Digital Currencies

5. Rules Risks and Online Safety

Despite promises of growth, doubts linger over whether PSV 2028 can reshape Nigeria’s digital future. Three years may reveal if ambition overtakes reality. Infrastructure gaps stand in the way. Cyber risks grow faster than safeguards. Rules pile up without clarity. Leadership falters under pressure. Success depends less on plans, more on execution. Past failures shadow current hopes. A nation watches, waiting for proof. Outcome uncertain.

The Evolution of Nigeria’s Digital Payments Journey From PSV 2020 to PSV 2028

Back then, over 60 out of every 100 grown-ups in Nigeria had no access to official money systems. Because machines that give cash were rare, payments took time to clear, which made using banks expensive. Not many branches existed in remote areas, so reaching one was tough for some. Worry about theft played a role too - people feared losing funds. On top of that, knowing how to use online tools stayed low across large parts of the population.

The CBN responded through a sequenced series of interventions:

|

Initiative |

Year |

Key Impact |

|

Payments System Vision 2020 |

2007 |

First strategic blueprint; established NIBSS and instant payment foundations |

|

Cashless Nigeria Initiative |

2012 |

Reduced cash dominance; encouraged POS and mobile money |

|

Payments System Vision 2025 |

2015–2025 |

Expanded electronic payments; introduced BVN; grew agent networks to 2 million; formal inclusion rose from 56% to 64% |

|

eNaira (CBDC) |

2021 |

First African CBDC; millions of wallets created (though adoption remains modest) |

|

Open Banking Framework |

2021–2023 |

Enabled API-based data sharing between banks and fintechs |

|

Regulatory Sandbox |

Ongoing |

30+ companies tested innovative products |

|

Agent Banking Expansion |

2018–2025 |

1.9–2.0 million agents across all LGAs |

By 2025, more people used digital tools and entered formal finance thanks to new programs. Under PSV 2025, those included in the financial system rose from 56 to 64 percent. Over time, enrollment in BVN passed 66 million Nigerians by July 2025. By October that year, nearly 124 million had registered for NIN. Roughly two million agents now deliver services where banks never reached before. Still, uneven cash supply and inconsistent service levels continue to challenge progress.

Nigeria’s Digital Payments Growth in Figures

What stands out today is just how big Nigeria’s shift toward digital payments has become. Evidence from the PSV 2028 report alongside figures provided by NIBSS reveals steady upward movement - rare among peers on the continent. Growth compounds year after year, visible in transaction volumes rising sharply. Few nations nearby show such consistent momentum. Numbers tell a clear story: expansion is real, measurable, ongoing.

Table 1: Growth Indicators in Nigeria's Digital Payments Ecosystem

Growth Indicators in Nigeria Digital Payments

|

Indicator |

2020 |

2025 |

|

Formal Financial Inclusion |

56% |

64% |

|

BVN Enrollment |

Below 50 million |

Above 66 million |

|

Agent Network |

Less than 500,000 |

About 2 million |

|

Electronic Payment Value |

Hundreds of trillions |

N1.2 Quadrillion |

|

POS Terminals Registered |

Limited penetration |

26.54 million registered |

|

Active POS Terminals |

~1.5 million |

~5.9 million |

Information comes from the CBN PSV report set for 2028, alongside data collected by NIBSS. Another key reference is the EFInA Access to Finance survey published in 2023. These documents together form the foundation of the analysis presented here.

MORE READ:

- The Cost of Distrust: How Nigeria's Credit Culture Is Killing SME Growth and Economic Development

- 5 Corporate Governance Failures That Cost African Companies Billions - And How to Avoid Them

- Why Africa’s Richest Nations Have Weak Currencies - What Nigeria Must Do Before 2027

- Nigeria - DRC Private Sector Partnership: A New Path for African Industrialisation and Economic Sovereignty

Table 2: Year-on-Year Electronic Payments Value Growth

Electronic Payments by Year Showing Value and Growth

|

Year |

Electronic Payments Value |

Growth Rate |

|

2022 |

N395.38 trillion |

— |

|

2023 |

N611.06 trillion |

+54.5% |

|

2024 |

N1.07 quadrillion |

+75.1% |

|

2025 (projected) |

N1.2 quadrillion |

+12.1% |

- Lagos International Financial Centre: Nigeria’s New Economic Blueprint

- How Corporate Governance Drives the Survival and Growth of Emerging Enterprises

- Why Strong Corporate Governance Is the Secret to African Business Survival

- Digital Governance in Nigeria, Why Corporate Boards Must Treat AI, Cybersecurity and Data Ethics as Fiduciary Duties

According to data from PSV 2028 published by NIBSS.

Table 3: Channel Distribution of Non-Cash Payments (Mid-2024)

Non Cash Payment Channels Mid 2024

|

Channel |

Share of Volume |

|

Web/Internet Transfers |

51.9% |

|

POS |

28.5% |

|

Mobile |

15.6% |

|

ATM |

2.2% |

|

Others |

1.8% |

What these figures show might surprise some: Nigeria has moved past planning for digital economic activity. The shift is already here. Now comes the real test - can systems handling data flows, rules guiding transactions, and public confidence grow fast enough to match what's happening on the ground?

The Five Key Areas Behind PSV 2028

Pillar One Infrastructure and Interoperability

Foundations matter most when it comes to payments. If systems fail, even strong ideas won’t hold up. Reliability isn’t optional - without steady operation, progress halts. Innovation alone cannot fix broken backbones. Consumer trust fades fast without consistency.

The Vision targets:

Almost every moment of operation is guaranteed - systems stay active through nearly all conditions. This level of reliability meets strict requirements for essential services. Rare interruptions, if any, fall within tightly controlled limits. Performance remains steady under pressure. Such consistency supports operations where downtime carries high risk

Most transactions succeed - fewer failures help maintain user confidence

- 100% ISO 20022 migration (global messaging standard for payments) by 2026

- Full interoperability among all licensed payment service providers (PSPs)

- Real-time payment capabilities nationwide, including underserved rural areas

What this means for companies cannot be ignored. When payments fail, problems follow - shoppers grow frustrated, money moves slower, running things gets costlier, work piles up, customers turn away from digital options. On online shopping sites, lifting successful transactions by just one percent adds up to billions of naira more income over time.

Payment systems that work well matter most when chasing debts, tracking assets, or guarding finances. A steady flow of transactions helps those who recover money move faster. When payments run smoothly, investigators find it easier to verify funds. Stability in transfers supports decision-making behind the scenes. Clear pathways in finance reduce delays during sensitive cases. Trust grows where processes do not break down. Efficiency often follows consistent backend performance

- Evidence trails for forensic analysis

- Verification of transactions supports resolution during conflicts

- Recovery efficiency through automated tracing

- Financial accountability across the ecosystem

Unreliable electricity supply still hampers progress across many regions, despite broader digital ambitions. Rural zones often face spotty internet access, limiting how widely new tools can spread. Point-of-sale terminals remain sparse where they are needed most. Even though the NIBSS Instant Payment platform works well, depending so heavily on one system raises concerns about resilience. Shifting toward the National Payment Stack aims to reduce such risks over time. This change needs careful handling, since interruptions could affect daily operations for millions. Progress here cannot come at the cost of stability already in place.

Pillar Two Digital Financial Inclusion Consumer Protection Financial Literacy

Still today, getting fair access to money tools counts among Nigeria’s top growth goals. Even with progress made, close to a quarter of working-age people cannot reach official banking help. Left out most are women, those living far from cities, plus folks earning pay without contracts. Though changes have come, gaps stay wide where they matter most.

PSV 2028 aims to:

By 2028, aim for 95 percent formal inclusion - starting from today’s 64. Progress follows steady policy shifts over time. One path includes broader access models across institutions. Growth becomes visible when systems adapt deliberately. Results depend on consistent implementation year after year. Ninety-five sits within reach - if momentum holds through each phase

- Raise digital payment usage from 52% to 80% of adults

- Starting small, reach remote areas by using local agents along with tools that work without internet. Different paths open doors where connectivity fails. One way builds on another, slowly closing gaps in service. Through these steps, isolated regions gain ground. Solutions adapt when signals fade. People benefit even far off the grid. Not every advance needs a network signal nearby

- Strengthen complaint resolution mechanisms through a unified redress portal

- Improve financial literacy nationwide, targeting schools, rural communities, and vulnerable groups

Despite progress, confidence remains fragile. A look into the PSV 2028 report reveals how deeply issues affect user experience. According to IPA's 2024 findings, four out of five people faced problems when accessing digital finance tools. Weak connectivity affected nearly half - specifically 44%. Meanwhile, hidden fees troubled 23%, just as often as scams did. In monetary terms, fraud drained N52.3 billion from users in one year alone. Yet by 2025, joint efforts across firms brought that figure down - to N25.85 billion, cutting harm almost in half.

One step toward fairness might be the new consumer redress portal paired with a financial ombudsman service. Right now, handling disputes spreads across too many players - banks send people to fintech firms who point back to telecom providers. When outcomes hinge on deadlines and decisions appear in public reports, confidence tends to grow. By 2028, under PSV goals, nearly all complaints should meet closure within set timelines while eight out of ten users report approval.

Economic Effects of Including More People in Financial Systems

Evidence repeatedly links broader financial access to stronger business creation, improved family earnings, more saving, clearer tax records, fewer people in hardship. In Nigeria, around 40 million small enterprises might grow if digital money tools were simpler to reach. Much of the economy outside official reporting - over half national output - still runs on physical currency. Moving such work onto electronic payment systems can sharpen revenue tracking, build borrowing backgrounds, allow precise public aid.

Pillar Three: Innovation, Digital Assets, and Emerging Technologies

PSV 2028 embraces a wide range of emerging technologies:

- Artificial Intelligence (AI) for fraud detection and credit scoring

- Blockchain for trade settlement and asset tokenization

- Open Banking APIs for data sharing and product innovation

- Digital Identity (BVN-NIN harmonization) for secure authentication

- Biometric Payments (fingerprint, facial, vein) for frictionless transactions

- Programmable Payments (smart contracts) for conditional transfers

- Stablecoins (fiat-collateralized) for cross-border remittances

- Digital Assets under clear regulatory frameworks

Right behind five others in the Chainalysis ranking, Nigeria shows strong movement into cryptocurrency territory. A large number of people use these systems every single week. From mid-2024 through mid-2025, money moving across borders probably added up to many billions of dollars. Because so much activity is already happening, officials now lean more toward managing it than shutting it down. Exclusion takes a back seat when real-world activity proves otherwise.

Among African countries, Nigeria could become an early adopter of clear digital asset rules through the PSV 2028 plan. Instead of grouping all stablecoins together, it suggests separating them into three kinds. One type relies on government-issued currencies, allowed only with central bank supervision. Another ties value to physical commodities, though access requires securities commission consent. The third kind uses automated systems to manage supply - these face a complete ban. Such distinctions might set a precedent across the continent.

One step ahead, Nigeria shows it still aims to lead in fintech through bold signals to investors. Still, progress stumbles as eNaira uptake drags behind due to shallow involvement of key players during its build and rollout. Missing coordination efforts further weaken momentum, while public understanding lags because outreach lies outside central bank priorities. What stands out emerges quietly, a clever idea collapses when those around it do not lean in.

Pillar Four Cross Border Payments And CBDC Integration

Despite progress, moving money across African borders remains a challenge for commerce. About two out of every three dollars sent home go through at least one costly shift in value before reaching their destination. Settlements often take days rather than hours, dragging down business speed. Instead of smooth transfers, firms deal with stacked conversions that chip away profits. Exchange hurdles pile up where systems fail to connect clearly. On average, fees hit 6.6 percent - more than double what global goals suggest they should be by now.

PSV 2028 proposes stronger integration with:

- PAPSS enables instant payments in local currencies across more than fifteen African nations

- AfCFTA digital trade platforms for harmonized trade documentation

- CBDC networks link Ghana South Africa and more

- Regulated stablecoin frameworks for cross-border remittances

One major effect stands out. Cross-border transactions that move quickly and cost less help boost exports - especially for food processors and factories. While Nigeria took in close to $21.8 billion through migrant money transfers in 2025, these improvements also lift remittances. Trade within Africa gains strength under the AfCFTA deal because of them. Foreign investors tend to follow such progress too. By 2027, the goal is to see official digital channels handle three-quarters of all remittances. Another target under PSV 2028 aims to push typical transfer fees down to 5 percent or lower.

Despite its launch, the eNaira remains barely used - only a tiny fraction circulates compared to cash by early 2024. If it stays isolated, cutting remittance or settlement fees won’t happen. Bridging systems through cross-border test runs becomes essential under such conditions. Pilot programs linking Nigeria with Ghana and South Africa could offer starting points. These would follow guidelines set by global institutions like the BIS and IMF on how digital currencies connect. Progress hinges less on technology alone, more on cooperation across borders.

Pillar Five Regulation Risk Management Cybersecurity

Security online might be the key foundation. With more payments happening daily, risks of scams rise at a much faster rate. The plan points out serious dangers like stolen identities, fake emails tricking users, manipulation through human interaction, money moved without approval, phone number hijacking, along with broad digital invasions.

The framework proposes:

- National Payment Security Operations Centre for continuous real time oversight

- Fraud intelligence sharing platforms across banks, fintechs, and telcos

- Tracking CISA Cyber Performance Goals Across Industries

- Stronger compliance frameworks with automated supervisory technology (SupTech)

Surprisingly, the numbers on fraud within PSV 2028 tell a clear story. From 2020 to 2024, financial losses due to deception jumped 350.2 percent. Most cases occurred through digital means especially mobile and internet platforms where tactics like phishing thrived alongside SIM swapping, unauthorized access to accounts, also internal cooperation played roles. By 2025, one region stood out: Lagos State faced 63 percent of such monetary damage, pointing toward high transaction volumes paired with dense exposure. Though nationwide issues exist, this area bore the brunt.

A sharp drop of 51 percent in reported fraud losses between 2024 and 2025 suggests efforts made across agencies are having an effect. By contrast, the Payment System Vision 2028 aims to shrink such incidents another 70 percent before that deadline. Detection now focuses on speed, with systems expected to flag issues within one hour. Fixes must follow swiftly, ideally resolved in under a day. Progress hinges less on isolated moves than sustained coordination.

Security of money flows marks a turning point in how Nigeria updates its financial backbone. Far beyond bank operations, protection of payments ties directly to safety of the nation itself.

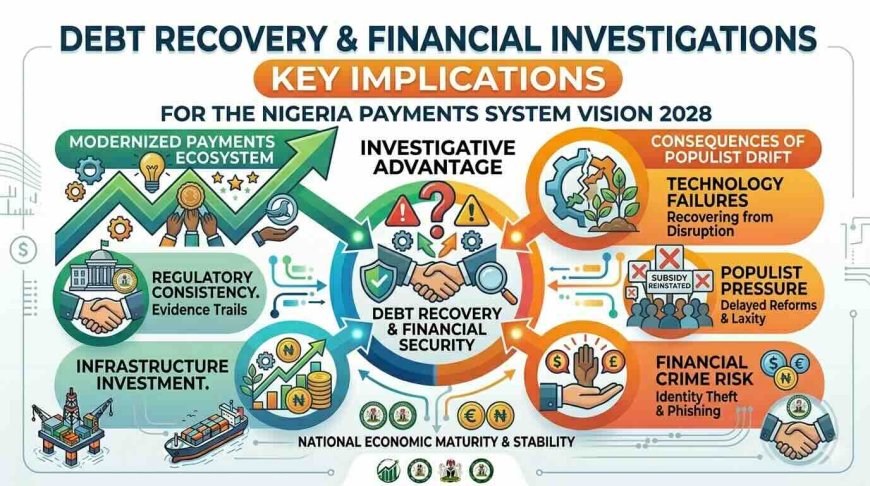

Debt Recovery and Financial Investigations Implications

Payment systems are shifting, opening fresh paths for those recovering debts. As BVN links up with NIN and digital ID structures, hidden activity fades. Interconnected payment routes make tracking easier. Financial behavior becomes more visible, less shielded. Accountability grows where gaps once existed. Anonymity shrinks under wider oversight.

Debt Recovery Operations Affected

Table 4: Impact on Debt Recovery Operations

|

Area |

Traditional System |

Digital Payment System (PSV 2028 Target) |

|

Transaction Tracing |

Difficult, manual |

Easier, automated, real-time |

|

Evidence Gathering |

Paper-based, slow |

Digital, timestamped, court-admissible |

|

Identity Verification |

Weak, easily falsified |

Strong, biometric, BVN-NIN linked |

|

Fraud Detection |

Reactive, after loss |

Proactive, AI-driven, real-time |

|

Asset Tracking |

Limited, fragmented |

Improved, cross-institutional |

|

Recovery Efficiency |

Slow, high cost |

Faster, lower cost, automated |

Because of these changes, skip tracing becomes more effective for debt collectors, private detectives, and finance watchdogs. Asset searches now yield clearer results, while finding debtors grows less complicated. Transaction histories are easier to rebuild, aiding probes into suspicious activity. Instead of working in isolation, a new alliance - formed by CBN, NIBSS, EFCC, and industry players - aims to unify efforts against scams. Every three months, performance updates will be shared publicly. These reports should make oversight stronger, showing who does what across the network.

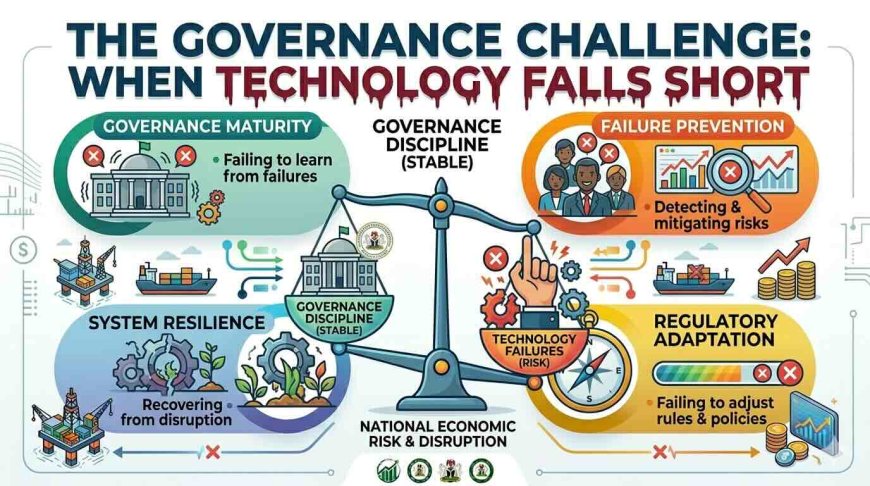

The Governance Challenge When Technology Falls Short

Success isn’t automatic just because tools improve. What really shapes PSV 2028’s outcome is how well decisions are made. Though tech matters, the real hurdles lie within systems - rules, roles, trust. These gaps aren’t fixed by machines

Infrastructure deficiencies (power, internet, last-mile connectivity)

Regulatory Complexity Across CBN SEC FCCPC NDPC NIMC NCC

Just a third of grown-ups manage to get three out of four basic money questions right. That gap in understanding shapes how people handle their finances day to day. A shaky grasp on fundamentals opens doors to poor choices later on. Without clear insight, confusion grows quietly over time. Mistakes pile up where guidance is missing. Confidence fades when knowledge runs thin. Fewer tools mean fewer options during tough moments

- Cybersecurity risks (evolving fraud techniques, insider threats)

- Weak connectivity in rural communities (broadband penetration below 50%)

Without strong governance:

- Investments become wasted on duplicative or incompatible systems

- Criminals take advantage of weak rules, making fraud more likely. When oversight falls short, dishonest actions find room to grow. Gaps in regulations become openings for misuse. As enforcement lags, deceptive practices spread. Loopholes invite manipulation. Where controls are thin, illegal behavior thrives

- Public trust declines when redress mechanisms fail

- Despite initial uptake, reliance on digital payments decreases when people return to physical money

Still, corporate oversight matters just as much as new tech. A setup for PSV 2028 includes a lead group guided by the central bank chief, expert teams focused on separate goals, along with an administrative hub placed inside the CBN’s payment policy unit. On charts and documents, it looks solid - yet real success hinges on overcoming Nigeria’s long-standing issue: getting different offices to work together when priorities clash and responsibility often fades. Though planned well, execution may stumble where cooperation lacks teeth.

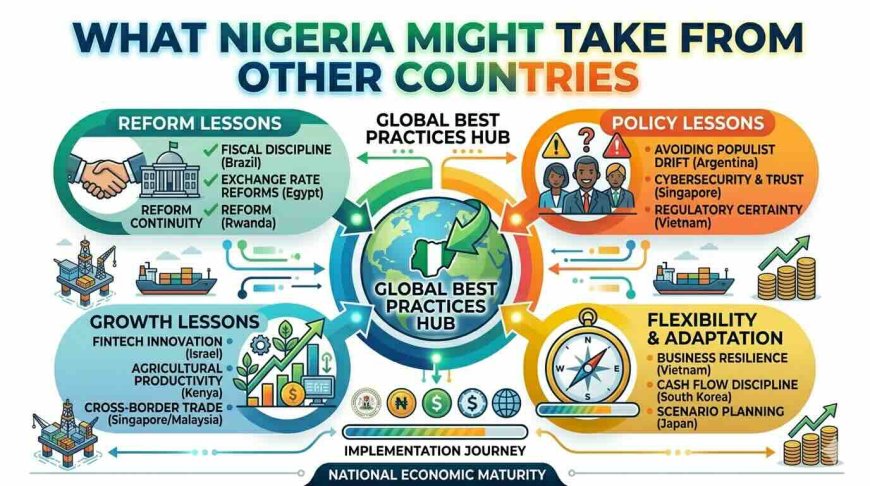

What Nigeria Might Take From Other Countries

Several countries provide useful benchmarks for Nigeria's journey.

What began as a government-backed initiative quickly gained momentum when banks and fintech firms joined forces. Backed by strict rules ensuring cross-platform compatibility, money moved freely across apps overnight. Small vendors welcomed fee-free handling of tiny digital payments - a shift few saw coming. Today more than ten billion such transfers happen every month without pause. Proof emerges not from theory but real-world traction - when policy aligns with cooperation, growth follows an unpredictable curve.

Surprisingly fast uptake across Brazil with more than 150 million people in just twenty-four months came through PIX, a payment tool built on instant transfers at zero cost. Easy sign-up helped, yet strong backing from the central authority played an equal role. Speed counts, but so does pricing; when moving money digitally beats handing over bills or swiping plastic, behavior shifts. Free access tilts the balance. People notice differences that save time, plus reduce effort.

Midnight payments move freely across Singapore’s network, showing how constant settlement systems support modern finance. Instead of waiting, money flows without delay thanks to round-the-clock gross processing. Digital currency trials unfold quietly alongside traditional banking, testing what comes next. Connections beyond borders grow through shared infrastructure, not just policy talk. Being central in Asia’s financial flow means aligning with global norms - this does not happen by accident. Collaboration shapes access, opening doors that isolation would keep shut.

Nigeria holds strengths absent in several of those nations

More than 200 million people live here. That number also matches the count of mobile subscriptions. A vast group of users stays connected through phones. Numbers show how deeply phone access has spread across regions. Nearly everyone owns a device now. Population size supports wide communication networks. Mobile use mirrors demographic scale closely

Fintech companies thrive in Nigeria with major players like Flutterwave Paystack and Moniepoint among many others

Around nine out of ten adults own a mobile device. Access spreads widely across age groups. Most people carry phones daily. Ownership reaches deep into rural regions too. Nearly everyone stays within reach of a handset

- Entrepreneurial culture (youthful, tech-savvy, risk-taking)

- Large diaspora network (over 17 million Nigerians abroad, sending $21.8 billion annually)

Execution falls short not because resources are missing, but due to inconsistent follow-through. What holds progress back isn’t scarcity of tools, rather a gap in sustained effort. Missing is not equipment, instead steady application. Success stalls less from empty hands, more from wavering habits. Not the absence of means, but weak structure in doing. Failure lies not in unavailable materials, yet in unreliable practice.

Critical Success Factors for PSV 2028

Success hinges on five elements, drawn from the PSV 2028 report along with global data. One factor follows another, yet each holds equal weight. Where conditions improve, these points tend to appear. Though not guaranteed, their presence often marks progress. Each piece connects to the others, sometimes loosely, sometimes tight

1. Policy clarity matters most when people invest or create new things. When rules shift too often, confidence drops. Sudden crackdowns do more harm than good. Different agencies like CBN, SEC, FCCPC, and NDPC pulling in separate directions only adds confusion. Instead of acting alone, they need real coordination. A shared platform for decisions could help - but only if it actually works. Empty meetings change nothing.

2. Even basic transactions depend on steady electricity and online access. When the grid fails, advanced payment tech becomes useless - no matter how polished. Though aiming for 99.999% availability sounds impressive under PSV 2028, reaching that mark means spending heavily on emergency power sources. Multiple network paths must back up main links, yet plenty of providers hesitate at such costs. Real resilience demands preparation few are ready to fund.

3. Because trust shapes how widely systems get used, support for the planned National Payment Security Operations Centre needs to match its goals. Without enough funding or experts on board, coordination between organizations could stall - yet early signs show promise. A drop in fraud by more than half during 2025 proves progress happens when effort aligns with strategy. Still, those who commit digital theft keep changing tactics. Staying ahead means spending steadily, not just reacting after harm occurs.

4. Confidence shapes how people embrace new tools. Because understanding matters, PSV 2028 aims to weave money skills into classrooms, youth service programs, and local gatherings. Without grasping basics - like how interest builds or scams operate - people stay exposed, hesitant. When doubt lingers, trust fades. Learning these concepts isn’t optional; it’s protective.

5. Working together matters when banks, fintech firms, government overseers, phone networks, shop owners, local agents, and people who pay bills all take part. The PSV 2028 paper rightly puts teamwork at the center of its vision. Still, past efforts to fix Nigeria’s money system often broke down under stress from tired partners, rivalry between groups, or rules shaped by powerful interests. For cooperation to last, those involved need reasons to stay engaged, clear ways to make decisions, leaders who answer for results. Few gains stick without these pieces firmly in place. Trust grows slowly but vanishes fast when actions do not match words. Real progress shows up not just in plans, but in how fairly burdens and benefits are spread across players.

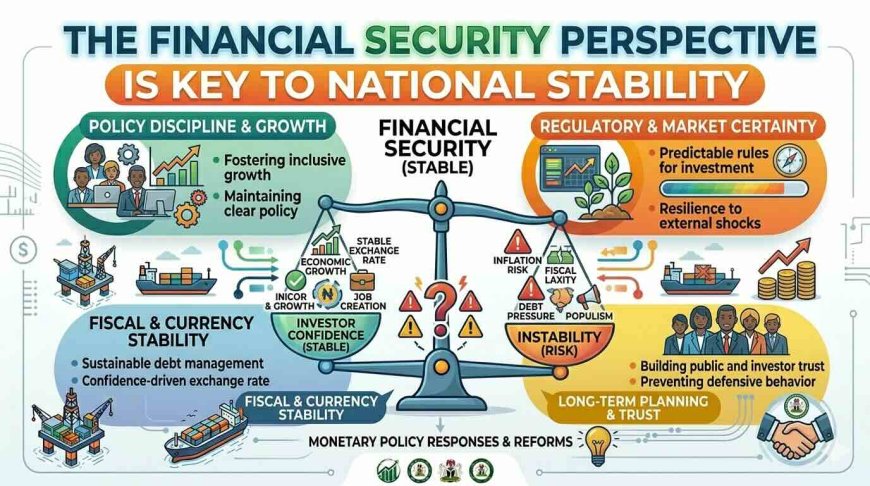

The Financial Security Perspective Is Key To National Stability

A secure payment system matters beyond bank concerns - its stability touches defense priorities. When money moves safely, so does trust in national infrastructure.

Faulty payment setups open doors to scams, illegal cash flows, bribery, funding of violent groups, along with broader economic crimes. Exiting the FATF grey list in 2025 marked progress, according to the PSV 2028 report. Still, holding that position depends on ongoing alertness across institutions. Rather than showing up only during audits, anti-money laundering and counter-terror finance rules need daily integration into how each payments provider functions.

Payment systems that work well help economies stay steady, boost trust among investors, improve how nations compete globally, while also making government operations more open. Because these benefits matter, efforts to build such systems must prioritize cyber safety and money protection right from the start - never tacking them on later as if they were mere formalities.

Economic Impact Forecast Success Defined

By 2028, assuming full rollout, PSV 2028 may bring notable financial gains - lasting well past that year. While uncertain, the scale of impact might grow steadily over time.

Table 5: Potential Economic Impact of PSV 2028

|

Impact Area |

Current Status (2025) |

Expected Outcome (2028) |

|

Financial Inclusion (formal) |

64% |

95% |

|

Digital Payment Usage (adults) |

52% |

80% |

|

MSME Digital Adoption |

~40% |

≥60% |

|

Government Revenue Collection |

Inefficient, cash-heavy |

Improved efficiency, transparency |

|

Foreign Investment in Fintech |

~$1-2 billion annually |

$10 billion+ targeted |

|

Job Creation |

Existing fintech jobs |

Significant new digital economy jobs |

|

Regional Trade Under AfCFTA |

Limited |

Stronger African integration |

|

Financial Transparency |

Improving |

Improved accountability |

Based on international evidence, countries with advanced digital payment systems typically experience higher GDP productivity (0.5-1.5% additional GDP growth), lower transaction costs (2-5% reduction in cost of capital), improved financial transparency (reduced leakage in government payments), and better investment attractiveness (higher fintech FDI multiples).

The Verdict On Whether To Take Or Lose?

The Nigeria Payments System Vision 2028 is one of the most ambitious financial infrastructure strategies ever developed in Nigeria. Its objectives extend beyond banking. The framework seeks to transform how Nigerians save, transact, invest, trade, receive remittances, access financial services, and participate in the digital economy.

The numbers already demonstrate significant progress. Electronic payment values have crossed N1.2 quadrillion. Financial inclusion has reached 74 percent (formal 64%). Digital identity enrollment continues to expand. Fintech innovation remains vibrant.

Yet the journey ahead is demanding. Infrastructure gaps, cyber threats, governance weaknesses, and regulatory complexity remain significant obstacles. The PSV 2028 document itself candidly acknowledges these challenges.

The ultimate success of PSV 2028 will not be measured by policy documents or technology deployments. It will be measured by whether ordinary Nigerians, businesses, investors, and institutions experience faster, safer, cheaper, and more inclusive financial services.

If implemented effectively, PSV 2028 has the potential to become the financial infrastructure foundation upon which Nigeria builds Africa's most competitive digital economy. If implemented poorly, it will join the long list of ambitious Nigerian policies that promised much and delivered little.

The difference between these two outcomes will be determined by three factors:

- Leadership accountability at the CBN and across implementing agencies

- Stakeholder alignment beyond the initial euphoria of the launch

- Resource commitment commensurate with the scale of the ambition

For policymakers, investors, financial institutions, fintech innovators, debt recovery professionals, and governance practitioners, the message is clear:

The future of Nigeria's economy will increasingly be shaped not by the movement of cash, but by the movement of digital value. PSV 2028 provides the roadmap. Whether Nigeria follows it or allows it to gather dust will define the next decade of economic development.

About the Author:

Standing at the intersection of strategy and financial oversight, Dr. Ohio O. Ojeagbase brings practical expertise into governance frameworks. Sourced directly from publicly available materials including the PSV 2028 blueprint, this piece unfolds without external influence. Whilst references guide its foundation, interpretation remains personal, shaped by individual analysis rather than collective stance.

Contact: report@probitasreport.com

Stay informed and ahead of the curve! Follow The Probitas Report on WhatsApp for real-time updates, breaking news, and exclusive content especially on integrity in business and financial fraud reporting. Don’t miss any headlines, connect with us on social media @probitasreport and visit www.probitasreport.com WhatsApp Only: +234 902 148 8737

[©2026 ProbitasReport - All Rights Reserved. Reproduction or redistribution requires explicit permission.]

Files

What's Your Reaction?