The Cost of Distrust: How Nigeria's Credit Culture Is Killing SME Growth and Economic Development

Nigeria's SMEs are struggling not only because of inflation and high interest rates, but because of a deepening crisis of trust. Explore how poor credit culture, rising loan defaults, and weak borrower accountability are damaging business growth and threatening the future of the economy.

By Dr Ohio O. Ojeagbase (Apostle Kreeno) -

Executive Summary

Nigeria's small and medium enterprises (SMEs) contribute 46% of GDP and employ 84% of the workforce (SMEDAN, 2023). Yet, 64% of Nigerian SMEs remain financially excluded - unable to access formal credit lines (EFInA Access to Financial Services Survey, 2023). The primary reason is not lack of capital in the system. It is a crisis of trust at micro lending level.

This article examines the economic cost of Nigeria's weak credit culture, the behavioral and structural drivers of loan default, and the urgent need for a national reorientation on borrowing and repayment as a matter of emergency and integrity, not mere convenience.

The Numbers: A Nation in Credit Distress

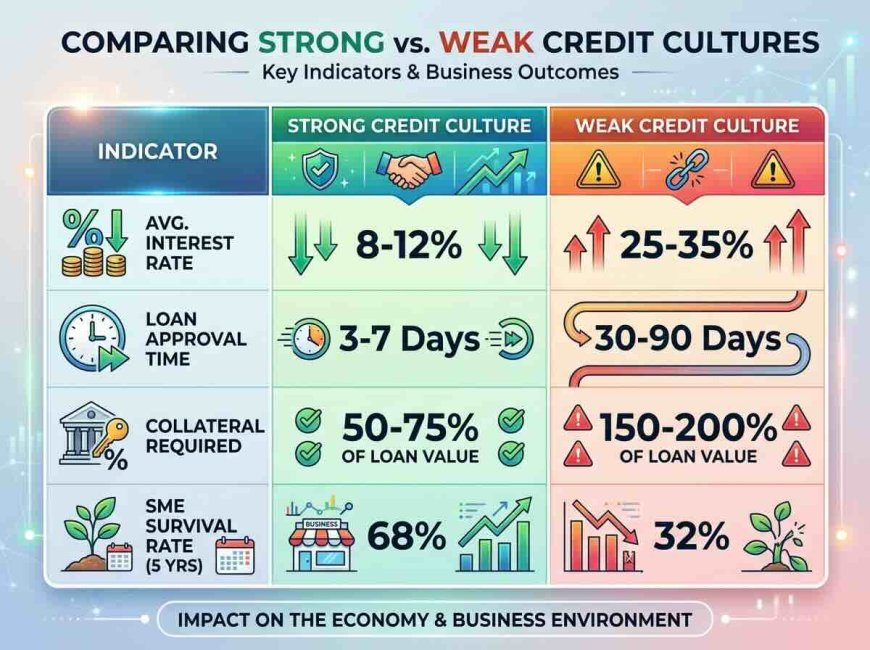

According to the Central Bank of Nigeria (CBN), the non-performing loans (NPL) ratio in Nigeria's banking sector stood at 33.8% as of Q4 2024 - well above the regulatory threshold of 5%. This means one in every three loans issued by Nigerian banks is in default.

The World Bank's 2024 Nigeria Development Update reports that credit to the private sector remains at 14% of GDP, compared to 45% in Kenya, 50% in South Africa, and over 100% in developed economies. The implication? Nigerian businesses are operating at a fraction of their potential capacity because capital is either unavailable or prohibitively expensive practically due to lack of integrity in business consciousness amongst business owners in Nigeria.

EFInA's 2023 survey reveals that 41% of Nigerian adults who were denied loans cited "poor credit history" as the reason. Another 28% were rejected due to "lack of collateral." But here's the paradox: Nigeria has over NGN 30 trillion in bank deposits (CBN, 2024) sitting idle because banks cannot deploy them responsibly.

The question is: Why?

The Root Causes: Beyond Economics to Ethics

1. Cultural Normalization of Default

In many Nigerian business circles, loan default is not stigmatized. It is sometimes even celebrated as "smart dealing." Phrases like "I no go pay again" or "Na bank get money" No be only me dey owe that interest rate is too much as it is against regulatory standard reflect a dangerous moral hazard - the belief that financial institutions are faceless entities that can absorb losses without consequence.

But the consequence is real. When one person defaults:

- Interest rates rise for everyone (banks price in risk)

- Credit lines shrink (banks tighten lending criteria to genuine businesses that have personnel that have sound corporate governance and integrity in business in their DNA)

- Collateral requirements increase (making credit inaccessible to the poor)

- Innovation stalls (entrepreneurs cannot scale without capital flowing and lenders tightens due to loan defaulters filled with excuses in their DNA)

A 2023 study by the International Finance Corporation (IFC) on credit culture in Sub-Saharan Africa found that every 1% increase in NPL ratios correlates with a 0.7% decrease in SME lending the following year. Default is not a victimless act.

2. Weak Enforcement Mechanisms

Nigeria's Credit Reporting Act (2017) established credit bureaus to track borrower behavior. Yet, enforcement remains very weak with delay in court proceedings. Only 38% of loan contracts are reported to credit bureaus (CBN Financial Inclusion Report, 2024), meaning defaulters can simply switch banks and borrow again under a clean slate or through proxies like Kreeno has discovered.

Compare this to the United States, where 95% of credit relationships are reported to the three major credit bureaus (Equifax, Experian, TransUnion). A default in the U.S. follows a borrower for 7-10 years, affecting their ability to rent housing, get employment, get accommodation, or obtain insurance.

Drawing lessons from Kenya's Credit Reference Bureau (CRB) system, which has reduced loan default rates by 22% since 2018 through mandatory reporting and enhanced credit transparency (Central Bank of Kenya, 2023), the Central Bank of Nigeria (CBN) should consider licensing and regulating specialized debt recovery intelligence and whistleblower entities such as KREENO Private Investigators. Empowering such accredited organizations with appropriate legal recognition, investigative support, and operational privileges could strengthen debt recovery mechanisms, improve credit culture, deter willful defaults, and enhance overall financial system stability.

Nigeria must ask: Why are we more lenient with financial dishonesty than our peers in Africa?

3. The "Government Example" Problem

When government agencies and politically exposed persons (PEPs) default on loans without consequence, it sends a devastating signal to the private sector and emerging entrepreneurs. The CBN's 2023 report noted that government-related entities account for 18% of all non-performing loans in the system.

If the federal and state governments do not honor their financial obligations to vendors and contractors, why should the citizens?

MORE READ:

- Why Africa’s Richest Nations Have Weak Currencies - What Nigeria Must Do Before 2027

- Nigeria - DRC Private Sector Partnership: A New Path for African Industrialisation and Economic Sovereignty

- Lagos International Financial Centre: Nigeria’s New Economic Blueprint

- How Corporate Governance Drives the Survival and Growth of Emerging Enterprises

- Why Strong Corporate Governance Is the Secret to African Business Survival

- Digital Governance in Nigeria, Why Corporate Boards Must Treat AI, Cybersecurity and Data Ethics as Fiduciary Duties

The Human Cost: SMEs as Collateral Damage

Case Study 1: The Manufacturer Who Couldn't Scale

Paul Iyare (name changed), a Lagos-based food processor, had a NGN 50 million loan approval in 2023 to expand his factory. But the bank collapsed the facility mid-disbursement when his supplier - who had received a separate NGN 20 million input loan - defaulted and triggered a sector-wide risk review.

Paul's business remained at 40% capacity. He could not hire 30 planned workers. He could not export. His story is replicated thousands of times across Nigeria - responsible borrowers punished by the irresponsibility of others.

Case Study 2: The Woman Who Paid - and Paid Again

Funke Adeyemi, a textile trader in Aba, repaid her NGN 5 million microfinance loan over 18 months at 28% interest. When she applied for a larger facility, she was quoted 35% - because the bank's risk model had adjusted upward due to industry-wide defaults in her sector.

She was being penalized for other people's dishonesty.

The Global Evidence: What Works Elsewhere

1. Germany's "Mittelstand" Model

Germany's SME sector - the Mittelstand - is the backbone of its economy. A key reason for its success? A culture of credit honor. German banks report NPL ratios below 3%, compared to Nigeria's 33.8%.

Why? Because default is socially unacceptable. Business associations enforce peer to peer accountability, and creditworthiness is tied to personal reputation in the community. Nigeria should emulate this approach.

2. Singapore's Integrated Credit Infrastructure

Singapore's Credit Bureau of Singapore (CBS) integrates data from over 1,000 financial institutions, utilities, telcos, and even rental payments. A citizen's credit score affects everything from loan approval to employment eligibility.

Result? Singapore ranks 2nd globally on the World Bank's *Ease of Getting Credit* index. Nigeria ranks 146th out of 190 countries.

3. Rwanda's Rapid Credit Reform

In 2015, Rwanda had an NPL ratio of 12%. By 2023, it had dropped to 4.2%. How? The National Bank of Rwanda mandated real-time credit reporting, introduced unique borrower IDs, and imposed criminal penalties for fraudulent defaul. At this juncture, Dr Ohio O.. Ojeagbase proposes this measure to both private and public borrowers whether reported to credit bureaus or law enforcement agency or in our courts. Court must also not waste time in dispensing justice when matters of breach on contract is brought to their courts for prompt conclusion of cases of such magnitude.

Rwanda proved that credit culture can be transformed within a decade - with political will.

The Biblical Imperative: Debt as Covenant

For the 70% of Nigerians who identify as Christian (Pew Research, 2023), and the 50% who are Muslim, there is a theological dimension to this crisis.

Psalm 37:21 declares: "The wicked borrows and does not repay, but the righteous shows mercy and gives." This is not a suggestion; it is a moral classification. Default is not merely a financial act - it is a spiritual condition.

In Deuteronomy 24:10-13, God establishes laws around borrowing and collateral, emphasizing dignity, fairness, and honor in financial relationships. The borrower is not a victim; the lender is not an enemy. Both are image-bearers of God, and the transaction must reflect that.

Proverbs 22:7 warns: "The rich rules over the poor, and the borrower is servant to the lender." This is not an endorsement of debt slavery, but a warning - debt creates dependency. To default is to reject responsibility for that dependency.

The Economic Case: Why Integrity-In-Business Pays

A 2024 McKinsey & Company report on African financial markets found that countries with strong credit cultures enjoy:

Integrity-in-business is not a moral luxury. It is an economic competitive advantage.

Recommendations: A National Call to Action

For Government & Regulators:

1. Mandate 100% credit reporting - All loans above NGN 100,000 must be reported to licensed bureaus within 7 days.

2. Enforce consequences for default - Include credit offenses in the Economic and Financial Crimes Commission (EFCC) mandate, ICPC, and Special Task Forces Against Financial Fraud.

3. Lead by example - Government agencies must maintain zero-tolerance on loan default.

4.Create a National Credit Honor Charter - A public commitment signed by banks, businesses, and trade associations.

For Financial Institutions:

1. Share data openly - Break down competitive silos on credit information.

2. Price risk fairly - Reward good borrowers with lower rates, not penalize them for others' defaults.

3. Invest in financial literacy - Educate borrowers on the long-term cost of default.

For Businesses & Entrepreneurs:

1. Treat debt as covenant - Not a contract to exploit, but a promise to honor.

2. Build credit intentionally - Your credit score is your economic passport.

3. Create peer accountability groups - Industry associations should self-police default behavior.

For Faith Communities: Restoring Financial Integrity as a Spiritual and Economic Imperative

Faith communities occupy a unique position of influence in shaping values, character, and societal behavior. Therefore, the challenge of loan defaults, credit indiscipline, and financial irresponsibility should not be viewed merely as an economic or banking issue; it is fundamentally a moral, ethical, and kingdom issue. Religious institutions must play a leading role in rebuilding a culture of trust, accountability, and financial stewardship.

1. Consistently Teach and Preach Financial Integrity

Financial integrity should become a regular component of discipleship and leadership teachings. Scriptures emphasize honesty, honoring commitments, stewardship, and the importance of maintaining a good name above material wealth. Faith leaders must boldly address issues such as willful loan defaults, fraudulent borrowing, breach of contractual obligations, and financial deception.

The erosion of trust in the financial system is not solely the responsibility of governments, regulators, and financial institutions. Faith communities must also accept their role in shaping the attitudes and behaviors of their members. A society that neglects financial ethics inevitably suffers from weakened trust, higher costs of doing business, and slower economic growth.

2. Establish Financial Literacy and Borrower Support Ministries

Many individuals fall into debt traps not because of dishonesty but because of poor financial planning, inadequate financial education, or unforeseen economic challenges. Faith-based organizations should establish financial counseling and borrower support initiatives to help members make informed borrowing decisions, manage debt responsibly, create realistic repayment plans, and build sustainable wealth.

Such ministries can provide guidance on budgeting, savings, investment principles, debt management, entrepreneurship, and responsible credit utilization. Preventing financial distress is often more effective than attempting to resolve it after it has become a crisis.

3. Model Honor, Accountability, and Transparency in Financial Dealings

Religious institutions must lead by example. Churches, ministries, mosques, and faith-based organizations should demonstrate the highest standards of financial accountability in all their transactions. Whether borrowing funds, engaging contractors, purchasing goods and services, or entering business partnerships, they must honor their obligations promptly and transparently.

Faith communities cannot effectively preach integrity while tolerating financial misconduct within their own structures. They must be known as institutions whose word can be trusted and whose commitments are fulfilled without excuses or delays.

4. Promote Reconciliation and Ethical Debt Resolution

Faith communities should serve as mediators and peacemakers in financial disputes where appropriate. Rather than encouraging avoidance or evasion of obligations, they should facilitate constructive dialogue between debtors and creditors, helping parties arrive at fair repayment arrangements and mutually beneficial resolutions.

This approach not only preserves relationships but also reinforces the principle that financial obligations are matters of honor and stewardship.

5. Build a Culture Where Reputation Is Treasured as Capital

A healthy credit culture begins with a healthy value system. Faith communities should teach that a person's reputation is one of their greatest assets. In both Scripture and society, trust is a form of capital. When individuals consistently honor their commitments, opportunities increase, partnerships flourish, and economic prosperity follows.

The restoration of Nigeria's credit culture will require more than legislation and regulation. It will require a moral and spiritual awakening in which faith communities actively champion integrity-in-business sermons, responsibility, accountability, and trustworthiness as core values of both faith and citizenship.

Conclusion: The Choice Before Us

Nigeria stands at a defining moment in its economic journey. We can continue along the path of credit indiscipline, where loan defaults are normalized, non-performing loan write-offs are celebrated as routine business outcomes, trust is eroded, and the cost of capital continues to rise. Or we can embrace a higher standard founded on integrity, accountability, and responsible financial conduct, where commitments are honored, reputation becomes a valuable asset, and businesses are empowered to grow and prosper.

The Probitas Report is advocating for a national reawakening in our approach to borrowing, lending, and trust. This conversation extends far beyond economics and finance; it speaks to our values, our character, and the kind of nation we aspire to build. A culture of credit responsibility is ultimately a culture of integrity, and integrity remains the foundation of sustainable economic development, investor confidence, and national prosperity.

Proverbs 11:1 says: "A false balance is an abomination to the Lord, but a just weight is His delight."

- Let us choose the just weight.

- Let us build a trust-proof economy and trust-proof ecosystem.

- Let us leave a legacy of honor for the next generation.

References

- Central Bank of Nigeria. "Statistical Bulletin Q4 2024."

- EFInA. "Access to Financial Services in Nigeria Survey 2023."

- SMEDAN. "National Survey of MSMEs in Nigeria 2023."

- World Bank. "Nigeria Development Update 2024."

- International Finance Corporation. "Credit Culture in Sub-Saharan Africa." 2023.

- McKinsey & Company. "African Financial Markets: The Integrity Dividend." 2024.

- Credit Bureau of Singapore. "Annual Report 2023."

- National Bank of Rwanda. "Financial Sector Performance Report 2023."

- Scripture quotations: NKJV.

Contact: report@probitasreport.com

Stay informed and ahead of the curve! Follow The Probitas Report on WhatsApp for real-time updates, breaking news, and exclusive content especially on integrity in business and financial fraud reporting. Don’t miss any headlines, connect with us on social media @probitasreport and visit www.probitasreport.com WhatsApp Only: +234 902 148 8737

[©2026 ProbitasReport - All Rights Reserved. Reproduction or redistribution requires explicit permission.]

What's Your Reaction?