Nigeria's Iron Ore and Steel Industry: Lessons from Germany's Industrial Success

Explore why Nigeria's iron ore and steel industry has struggled despite abundant mineral resources. This comparative analysis examines Nigeria's steel sector alongside Germany's successful industrial model, highlighting lessons for economic diversification, industrialisation, and sustainable national development.

It is a universally accepted fact that iron and steel production forms the bedrock of the industrial revolution. Its applications span across vital economic sectors, serving primarily to bind or reinforce materials within the construction industry. Nations devoid of these natural resources must depend heavily on imports to mitigate local deficits or non-availability.

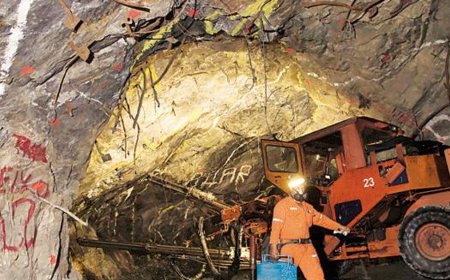

Conversely, Nigeria is richly endowed with vast mineral wealth, possessing an estimated 2 to 3 billion metric tons of iron ore reserves. Driven by a strategic vision to diversify its economy away from oil dependency and build a resilient industrial base, Nigeria embarked on ambitious, large-scale iron and steel projects. These included the Ajaokuta Steel Complex, the Delta Steel Company at Aladja, and the National Iron Ore Mining Company (NIOMCO) at Itakpe. Unfortunately, this giant leap has failed to yield the desired developmental results.

History demonstrates that nations capable of successfully harnessing their iron and steel deposits—such as Germany, South Korea, Japan, and the United States—transform into industrial giants. Many nations lacking this endowment either remain largely underdeveloped or must aggressively explore alternative markets.

Nigeria's case is particularly peculiar: despite sitting on top of massive reserves and ranking 7th globally in iron ore deposits, the country has yet to effectively mine the ore, squandering its immense industrial potential. Over five decades, Nigeria has spent upwards of $10 billion attempting to establish a domestic steel industry, yet it remains a net importer, spending approximately $4 billion annually on foreign steel imports. In stark contrast, Germany—operating with fewer raw reserves—is the largest steel producer in the European Union and an industrial powerhouse.

This article investigates how iron ore acted as a transformative catalyst in Germany and why similar attempts by Nigeria failed. It explores the foundational economic theories governing mineral-led development, analyzes the causes of failure across Nigeria’s primary steel infrastructure, and outlines potential strategic pathways for revival.

Nanya - Miss Probitas Report

Economic Framework: Linkages vs. The Resource Curse

To understand this disparity, two contrasting economic frameworks must be considered:

· Linkage Theory (Hirschman, 1958): Postulates that iron ore generates powerful backward linkages (stimulating demand for mining equipment, energy, and transport infrastructure) and forward linkages (feeding into steel production, manufacturing, and construction). This structural interdependence creates a robust multiplier effect throughout the broader economy. Early industrialized countries converted raw mineral wealth into high-value manufactured goods, capturing escalating economic value at every stage of production.

· The Resource Curse (Auty, 1993): Conversely, countries that export raw minerals without adding value often fall victim to the "resource curse". This phenomenon is characterized by the Dutch disease, institutional decay, systemic corruption, and a persistent failure to diversify. The missing link for development is not the physical presence of iron ore, but rather the domestic capacity to convert raw minerals into finished industrial output.

The German Experience: A Model of Industrial Transformation

The German industrial revolution (1840s–1870s) was anchored in the Ruhr Valley, a region naturally endowed with rich coal deposits located in close geographic proximity to the iron ore reserves of Siegerland and Lorraine (situated between France and Luxembourg). Rather than relying on market forces alone, German industrialization was state-directed, technologically sophisticated, and systematically planned.

Key Historical Milestones in German Steel Development

|

Period |

Development and Milestones |

|

1840s |

Operationalization of the first coke-blast furnaces in the Ruhr; commencement of rapid railway network expansion. |

|

1871 |

German unification; establishment of coordinated national industrial policies. |

|

1873 |

National steel production reaches 3.3 million tonnes. |

|

1880 |

National steel production rises to 6.5 million tonnes. |

|

1893 |

Germany officially surpasses Great Britain in total crude steel output. |

|

1900 |

Crude steel production reaches 7.5 million tonnes. |

|

1950s |

The post-WWII Marshall Plan actively supports the revival and modernization of the steel sector. |

|

1974 |

Peak German steel production reaches 53 million tonnes. |

|

2022 |

Production stands at 36.9 million tonnes, supporting over 4 million jobs in steel-intensive sectors. |

Interconnecting Pillars of German Success

The Ruhr Valley’s transformation into the industrial epicenter of Europe relied on a highly integrated ecosystem characterized by five core pillars:

1. Institutional and Financial Backing: Germany established solid industrial banks (such as Deutsche Bank and Dresdner Bank), technical universities (Technische Hochschulen), and industry associations (Verbände). These three entities coordinated long-term capital investment, cutting-edge research, and specialized labor training.

2. Vertical Integration: Major German industrial firms like Krupp, Thyssen, and Hoesch achieved full vertical integration. They controlled every stage of the value chain—from iron ore mining and pig iron smelting to final steel manufacturing—thereby maximizing domestic value addition.

3. State-Industry Symbiosis: During the Bismarck era, the state actively protected domestic industries through protective tariffs and heavily subsidized transport infrastructure, including extensive networks of railways and canals that linked mines directly to production mills and commercial markets.

4. Technological Innovation: Germany aggressively adopted and refined pioneering metallurgical technologies. They implemented the Bessemer process (1856), the Siemens-Martin open-hearth furnace (1860s), and the Thomas-Gilchrist basic process (1878). The Thomas-Gilchrist process specifically allowed Germany to utilize the highly phosphoric iron ores of Lorraine, a technical feat that British mills of the era could not replicate.

5. Human Capital and the Dual Apprenticeship System: Recognizing that an industrial sector is only as strong as its workforce, Germany instituted a nationally coordinated dual apprenticeship system (Berufsausbildung). This system systematically generated a highly skilled, technically competent workforce capable of operating advanced industrial processes.

Economic Impact of the German Steel Industry (2022–2023)

|

Indicator |

Economic Value / Impact |

|

Crude Steel Production (2022) |

36.9 million tonnes. |

|

Direct Steel Industry Employment |

78,000 workers. |

|

Employment in Steel-Intensive Sectors |

4,000,000 workers. |

|

Contribution to Manufacturing GDP |

23%. |

|

Steel Sector Revenue Growth (2022) |

+13.8 billion Euros. |

|

Ruhr Region GDP (2021) |

180.5 billion Euros. |

|

European Union Production Rank |

Largest steel producer in the EU. |

This robust structural base created far-reaching forward integration. The domestic automotive industry (including brands like Volkswagen, BMW, and Mercedes-Benz) emerged as the primary consumer of German steel, ensuring reliable local demand. Furthermore, the engineering and machinery giants (such as Siemens and Bosch), alongside defense and shipbuilding industries, drew heavily from this steel infrastructure, powering the German "economic miracle" of the 1950s and 1960s.

Nigeria's Steel Vision and the Three Pillars

While iron and steel catalyzed Germany's industrialization, Nigeria's extensive mineral endowments have yielded an entirely different outcome. Despite ranking highly in global reserves, Nigeria's actual development rate of these resources remains below 10%.

Nigeria's National Iron Ore Endowments

|

Deposit Location |

Estimated Reserves |

Grade (% Fe) / Status |

|

Itakpe, Kogi State |

3 billion tonnes |

36% Fe |

|

Agbaja Plateau, Kogi State |

401 million tonnes |

45% Fe |

|

Oshokoshoko |

Significant |

Moderate Grade |

|

Ajabanoko |

Significant |

Moderate Grade |

|

Total National Estimate |

+2–3 billion tonnes |

Variable Quality |

In 1979, the administration of President Shehu Shagari sought to harness these reserves by establishing an integrated domestic steel ecosystem via state decree. The strategy was designed as a closed-loop value chain: mine raw iron ore at Itakpe, process it into steel at the Ajaokuta blast furnace plant, utilize scrap and sponge iron at the Aladja Electric Arc Furnace, roll the intermediate steel at regional inland mills, and distribute the finished products to national construction and manufacturing markets.

The plan rested on three major pillars, all of which ultimately collapsed into dormancy.

1. Ajaokuta Steel Company Limited (ASCL)

Spanning 24,000 hectares in Kogi State, ASCL was designed as the largest integrated steel complex in sub-Saharan Africa, with an intended capacity of 5.2 million tonnes of steel per year. Construction began in 1979 using Soviet-backed blast furnace technology. By 1994, the project reached 98% structural completion, with 40 out of 43 functional units fully built.

Between 1979 and 1994, total capital expenditure reached an estimated $8 to $10 billion. Despite this massive investment, the complex never produced a single commercial sheet of steel. Instead, it became a fiscal drain, requiring an annual allocation of ₦6.69 billion (approximately $4.5 million) simply to pay the salaries of an idle workforce.

The management history of Ajaokuta shifted through successive waves of policy reversals:

· 1999: Concessioned to Kobe Steel of Japan, which failed to materialize.

· 2004: Concessioned to Global Infrastructure Holdings Limited (GIHL/Ispat).

· 2008: The Yar'Adua administration terminated the GIHL contract due to allegations of asset stripping.

· 2016: The Buhari administration spent $496 million in legal settlements to buy back the complex from GIHL, following a prior $650 million revival allocation by the Jonathan administration in 2010.

· 2019: A bilateral Memorandum of Understanding (MoU) signed between President Buhari and Russian President Vladimir Putin at the Russia-Africa Summit was derailed by the COVID-19 pandemic.

2. Delta Steel Company (DSC), Aladja

Located near Warri in Delta State, DSC was commissioned in 1982 with an Electric Arc Furnace (EAF) designed to produce 1.0 million tonnes of liquid steel per year using scrap metal and Direct Reduced Iron (DRI) sponge iron. It operated fitfully during the 1980s before falling completely dormant in 1995.

In 2005, the Bureau of Public Enterprises (BPE) privatized the asset, selling it to Global Steel Holdings Limited for a paltry $30 million—representing just 1.6% of its original $1.89 billion construction cost. This sale was widely criticized as a catastrophic undervaluation. In 2018, the asset was partially transitioned to Premium Steel and Mines Limited, but it continues to operate at minimal, negligible capacity.

3. National Iron Ore Mining Company (NIOMCO), Itakpe

NIOMCO was established to act as the primary upstream feed for the entire national steel ecosystem, specifically engineered to supply 600,000 tonnes of processed iron ore concentrate annually to Ajaokuta’s blast furnaces. Despite its multi-billion Naira funding allocations and a theoretical capacity to generate ₦72 billion ($49 million) in annual revenue, its operational history has been highly intermittent. NIOMCO has been largely inactive since 2008, leaving the country's massive iron ore reserves stranded underground.

Comparative Analysis and Financial Expenditures

The stark contrast between the outcomes of the German and Nigerian steel strategies highlights a deep divergence in execution, fiscal discipline, and institutional continuity.

Cost-Output Comparison: Germany vs. Nigeria

|

Indicator |

Germany |

Nigeria |

|

Total Sector Investment |

~$50 Billion (Cumulative lifetime) |

$13–$15 Billion (Sunk capital) |

|

Annual Crude Steel Output (2024) |

36.0 Million Metric Tonnes |

~0.2 Million Metric Tonnes |

|

Steel Output per $1B Invested |

High / Efficient |

Near Zero |

|

Trade Status / Dependency |

Net Exporter of Steel |

Net Importer (~$4B spent annually) |

|

Sector-Associated Employment |

~4,000,000 workers |

<50,000 workers (largely idle) |

|

Contribution to Manufacturing GDP |

23% |

Less than 1% |

|

Functional Integrated Plants |

Multiple operational complexes |

0 (Zero functional integrated plants) |

Financial Breakdown of Nigeria's Steel Sector Exposure

Total Estimated Government Investment Sunk: $13 – $15 Billion

· Ajaokuta Steel Complex (ASCL) Sunk Costs: $10–$12 Billion

o Original Soviet Contract (1979–1994): $2.4 Billion

o Jonathan Admin Revival Allocation (2010): $650 Million

o GIHL Legal Settlement/Buyback (2016): $496 Million

o Cumulative Idle Salaries (Past Decade): ₦38.9 Billion (~$26 Million)

· Delta Steel Company (DSC) Construction Cost: $1.89 Billion

· NIOMCO Itakpe Sunk Costs (Est.): $500 Million

· Inland Rolling Mills (Oshogbo, Jos, Katsina): $300–$500 Million

Nigeria's Annual Steel Import Expenditure (2018–2024)

Because domestic infrastructure remains non-functional, Nigeria’s dependency on foreign steel has steadily intensified, draining vital foreign exchange reserves.

2018: █ $2.8 Billion

2019: ██ $3.1 Billion

2020: █ $2.4 Billion (COVID-19 contraction)

2021: ███ $3.5 Billion

2022: ████ $3.8 Billion

2023: █████ $4.08 Billion

2024: █████ $4.08+ Billion

(Source: Sinosteel Pipe Overview 2024)

Core Causes of Nigeria's Industrial Failure

The systemic collapse of Nigeria's steel initiatives can be traced to seven interconnected structural, political, and economic factors:

· Political Instability and Regime Discontinuity: Between 1966 and 1999, Nigeria experienced seven military coups. This political volatility disrupted long-term industrial policy. Incoming administrations frequently abandoned the projects of their predecessors or withheld necessary funding, preventing any sustained developmental momentum.

· Systemic Corruption and Fund Diversion: Capital allocations intended for the completion and commissioning of Ajaokuta and related projects were systematically siphoned off by public officials. The projects were treated more as political instruments for financial rent-seeking than as strategic industrial priorities.

· Infrastructure and Raw Material Decoupling: A blast furnace requires an uninterrupted, continuous supply of processed iron ore, metallurgical coal, and electricity. Because NIOMCO failed to operate at capacity and the critical railway lines connecting Itakpe, Ajaokuta, and Warri remained uncompleted for decades, the logistical link was broken, and the primary furnace could never be safely ignited.

· Flawed Privatization and Asset Stripping: The concessions and subsequent privatization of ASCL and DSC to external managers between 2004 and 2008 lacked transparency. Rather than injecting fresh capital and upgrading systems, these arrangements resulted in widespread asset stripping, where vital operational equipment was dismantled and sold off.

· Technological Obsolescence: The Soviet blast furnace models implemented in 1979 grew technologically obsolete over decades of dormancy. Modernizing these systems to remain competitive with global steel markets now requires substantial injections of fresh capital that successive governments failed to commit.

· Human Capital and Technical Skill Gaps: Unlike Germany’s highly coordinated dual apprenticeship system, Nigeria failed to implement a structured, domestic framework for training engineers, metallurgists, and technical managers. This reliance on foreign technical expertise left local teams ill-equipped to independently maintain, troubleshoot, or manage the complexes.

· Managerial Political Interference: Leadership appointments at Delta Steel and Ajaokuta were frequently driven by political patronage rather than merit. Placing unqualified individuals in sensitive technical positions created severe managerial inefficiencies and operational stagnation.

Current Revival Initiatives and Projections

Between 2024 and 2026, the federal government initiated a series of fresh interventions and bilateral negotiations aimed at rehabilitating these moribund assets.

National Steel Sector Intervention Matrix (2024–2026)

|

Initiative / Project |

Bilateral Partner |

Value |

Operational Status (2025–2026) |

|

TPE / Novastal MoU |

Russian Federation |

Est. $1.0–$1.5 Billion |

Signed September 2024; currently undergoing technical audit and plant assessment. |

|

Chinese Consortium Talks |

Luan Steel, Fangda, Jingye, Sinosteel |

$2.0 Billion |

Advanced negotiations underway; targeting long-term production of 10M tonnes/year. |

|

Stella Steel Plant (Ogun) |

Inner Galaxy Group |

$400 Million |

Groundbreaking concluded; formal commercial commissioning scheduled for April 2026. |

|

ASCL Rolling Mill Restart |

FGN / Private Consortium |

Partial Funding |

Targeted restart of the 1.3M Metric Tonne light section mill by late 2026. |

|

Premium Steel Revamp |

AMCON / Private Investors |

Undisclosed |

Minimal localized operations ongoing; structural reorganization underway. |

Future Steel Output Projections (2024–2035)

The Ministry of Steel Development has modeled three potential output trajectories (measured in million metric tonnes per year) based on the progress of current revival efforts:

· Base Case (Status Quo): Assumes minimal structural reforms and persistent technical stagnation, with output crawling from 0.20M tonnes in 2024 to just 2.00M tonnes by 2035.

· Moderate Growth Scenario: Assumes the successful reactivation of regional rolling mills and partial private concessions, reaching 5.00M tonnes by 2030 and 9.00M tonnes by 2035.

· Optimistic Growth Scenario: Assumes full, uninterrupted modernization and operationalization of Ajaokuta's core integrated blast furnace alongside NIOMCO, driving national production to 10.00M tonnes by 2030 and 15.00M tonnes by 2035.

· Here is the structured breakdown of the projection data from "THE NIGERIA FORAY INTO IRON ORE" presented in a clean, comparative table format:

National Steel Output Projections (2024–2035)

|

Target Year |

Base Case (Status Quo)(Million MT/Year) |

Moderate Scenario(Million MT/Year) |

Optimistic Scenario(Million MT/Year) |

|

2024 |

0.20 |

0.20 |

0.20 |

|

2026 |

0.50 |

1.30 |

3.00 |

|

2028 |

0.80 |

3.00 |

6.50 |

|

2030 |

1.20 |

5.00 |

10.00 |

|

2032 |

1.50 |

7.00 |

12.00 |

|

2035 |

2.00 |

9.00 |

15.00 |

· Note: As indicated in the source document, these targets are based on the Federal Ministry of Steel Development (FMoSD) models. The Optimistic Scenario rests entirely on the crucial assumption that the Ajaokuta Steel Complex is successfully rehabilitated and brought to its optimal, fully integrated production capacity.

Strategic Recommendations for Nigeria's Steel Revival

To escape the historical cycles of failed interventions, Nigeria must look to the proven structural tenets of the German model, adapting them to modern economic realities:

1. Establish an Autonomous Steel Development Authority: The management of the steel value chain must be completely insulated from political interference. Nigeria should establish an independent governing authority modeled after Germany's industry associations (Verbände) or South Korea's highly successful POSCO framework. This entity must be led strictly by merit-vetted metallurgical and financial experts rather than political appointees.

2. Enforce Absolute Ecosystem Integration: The steel sector cannot function as isolated units. The government must ensure the flawless, continuous operation of the Itakpe-Ajaokuta-Warri industrial rail corridor. NIOMCO must be operationally synchronized to feed ore directly into Ajaokuta, which in turn must provide intermediate feedstock to the regional rolling mills.

3. Secure Dedicated Energy Infrastructure: A primary reason for plant failure is power instability; an operational Electric Arc Furnace requires an uninterrupted supply of 400 to 600 Megawatts (MW) of electricity. The revival plans must include dedicated, off-grid power generation assets specifically allocated to the Aladja and Ajaokuta complexes.

4. Codify Binding Performance Milestones into Law: Drawing from the costly lessons of the 2004–2008 GIHL concession, any future public-private partnerships or concessions must include strict, legally binding production targets. Failure to hit these specific technical milestones must trigger immediate, automated financial penalties and contract termination clauses to prevent asset stripping.

5. Institutionalize National Human Capital Development: Nigeria must build local engineering self-reliance. Specialized steel manufacturing, metallurgy, and heavy industrial automation curricula should be integrated into national tertiary education frameworks. Furthermore, bilateral agreements should include mandatory technical transfer clauses, such as sending cohorts of local engineers to specialized steel training institutions like those in Duisburg, Germany.

6. Capitalize on Regional Trade Integration: The domestic market alone presents a guaranteed demand estimated at $10 billion annually. By successfully reviving its steel sector, Nigeria can use the framework of the African Continental Free Trade Area (AfCFTA) to position itself as the primary supplier for the broader $300+ billion African construction and infrastructure market. This would effectively transform the nation from a vulnerable, resource-cursed importer into a dominant, self-sustaining industrial hub across sub-Saharan Africa.

About Probitas Report

Probitas Report is a publication dedicated to promoting integrity in business, leadership excellence, sustainable development, corporate governance, innovation, and transformational initiatives that advance national growth and global competitiveness.

Contact: report@probitasreport.com

Stay informed and ahead of the curve! Follow The Probitas Report on WhatsApp for real-time updates, breaking news, and exclusive content especially on integrity in business and financial fraud reporting. Don’t miss any headlines, connect with us on social media @probitasreport and visit www.probitasreport.com WhatsApp Only: +234 902 148 8737

[©2026 ProbitasReport - All Rights Reserved. Reproduction or redistribution requires explicit permission.]

What's Your Reaction?