Relational Governance Through Visionary Friendships: How Access Bank and Oando Built Bluechip African Multinationals

Explore how relational governance, visionary friendships, and strategic leadership shaped the rise of Access Bank Plc and Oando Plc into bluechip African multinationals through a comparative case analysis of corporate governance, partnerships, and expansion strategies.

Pre-Research Article 1

Relational Governance Through Visionary Friendships: Building Bluechip African Multinationals - A Comparative Case Analysis of Access Bank and Oando Group

OJEAGBASE Ohio Okhaide (PhD, FICA, SFIDR)

Probitas Report: Journal of Sustainable Business and Governance in Africa

Abstract

This article addresses a critical gap in the literature on African multinational enterprises (MNEs) by investigating how strategic partnerships among loyal friends sharing a vision for African liberation build bluechip companies. While existing scholarship has extensively documented general strategic alliances among African MNEs (e.g., MTN, Dangote) and examined institutional voids in emerging markets, no studies have specifically explored "loyal friend networks" as informal governance mechanisms that catalyze the journey to bluechip status. Drawing on social capital theory and network theory, this study conducts a comparative case analysis of two exemplar African corporations: Access Bank (current market capitalization ~$1.02 billion) and Oando Group. Starting with real numbers, company updates, and old records, this study builds an idea called vision-aligned relational governance. Trust built over years between founders acts like unofficial rules, helping firms move fast through shaky systems across Africa. Such bonds also open doors to major market shifts, even toward global-grade operations. By naming these ties - vision-aligned friend networks - the work adds fresh thinking to leadership studies and cross-border business research. Ideas here may quietly guide leaders and new builders in Africa who aim for steady scale without flash or noise.

Keywords: African Liberation and Relational Governance Through Friendship Networks in Bluechip Companies Like Access Bank and Oando Group Shaping Strategic Partnerships via Informal Institutions and Social Capital

1. Introduction

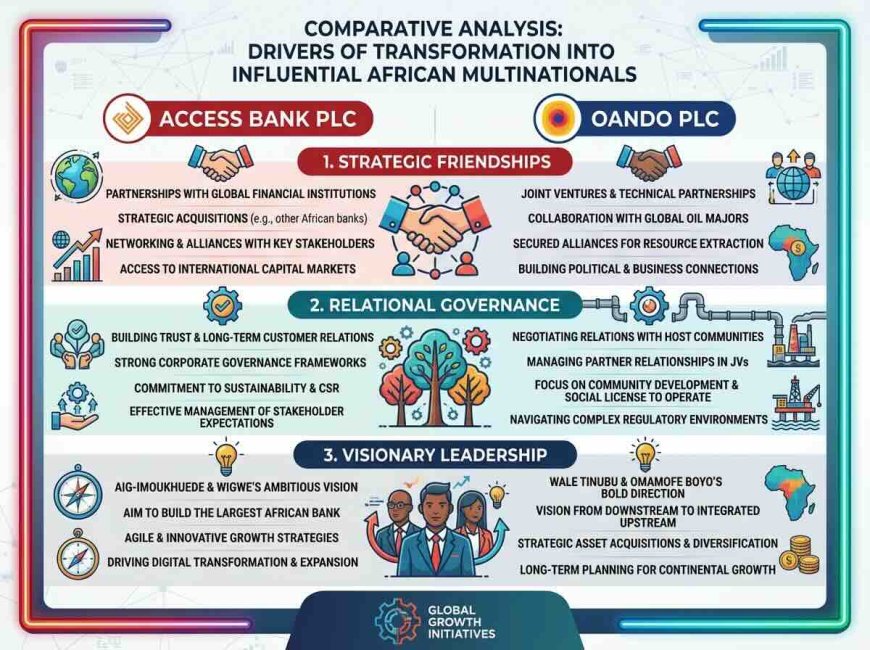

Back in 2002, a pair of Nigerian bankers - Aigboje Aig-Imoukhuede and Herbert Wigwe - took a leap using their own money, stacking loans on top, buying a fading 14-year-old institution named Access Bank. That bank held just ₦11.3 billion in assets, about $30 million then, placing it at number 65 out of 89 banks nationwide. Fast forward past twenty years, that once shaky firm now stretches across more than 25 African nations, standing tall as a major financial force. Its worth climbed to around ₦1.41 trillion, close to $1.02 billion, with holdings hitting ₦51.56 trillion, stepping firmly into blue-chip ranks. On the Nigerian Exchange, Oando PLC climbs quietly but surely up the list of top gainers. A local energy firm, it emerged from a partnership between Wale Tinubu and Omamofe Boyo, who’ve known each other for years. Under strain, most would have faltered - this one broke through. Now worth more than ₦1 trillion, it joined an elite group few reach. It ranks second among oil and gas firms by market value, surpassing companies backed by international capital.

What explains these extraordinary trajectories? Existing literature on African MNEs has largely focused on formal joint ventures, resource‑based strategies, and institutional voids. Standard accounts attribute Access Bank’s rise to strategic acquisitions and a disciplined expansion playbook, and Oando’s growth to its mid‑stream pact with Helios Investment Partners. While valuable, those accounts overlook a more fundamental driver: the loyal, decades‑long friendships between the controlling founders. Out of the blue, Aig-Imoukhuede crossed paths with Wigwe at Guaranty Trust Bank back in the 90s - ever since, their bond held strong through decades of joint ventures. When tragedy struck in 2024 with Wigwe's fatal helicopter crash, it marked the end of a lifelong alliance forged in finance. Meanwhile, Tinubu and Boyo took different roots but followed identical paths: same childhood, same classrooms, then later co-piloting Oando’s journey from modest fuel deals to broad energy reach. Though not written in bylaws, these ties function like quiet steering wheels behind big choices - trust replacing paperwork. Speed came easier because second guesses rarely entered the room. Risks felt smaller when two minds saw them as one. Vision? Always fixed on an Africa running its own economy, no outside strings. Decades rolled by, yet the compass never shifted.

This piece of article tackles a missing puzzle - though team-ups get plenty of attention in business studies, nearly nothing looks at tight-knit friend circles as engines pushing African companies toward top-tier success. Little has been said about how deep bonds, rooted in liberation dreams, link up with company results in developing economies like Nigeria. Into that quiet space steps this work, wondering: When founders carry old loyalties into their ventures, what happens to control and growth paths? What shifts when those ties come wrapped in a common hope for Africa’s rise?

The remainder of the article is structured as follows. Section 2 reviews the relevant theoretical and empirical literatures. Section 3 develops a conceptual framework for "vision‑aligned relational governance." Section 4 describes the research methodology. Section 5 presents comparative case findings for Access Bank and Oando Group. Section 6 discusses the theoretical and practical implications, and Section 7 concludes with research directions for the field.

2. Literature Review

This review is organised around four major streams: (a) strategic partnerships and firm performance in emerging markets; (b) social capital, friendship ties and informal governance; (c) institutional voids and the role of networks in sub‑Saharan Africa; and (d) bluechip transitions and African MNEs.

2.1 Strategic Partnerships in Emerging Markets

A well‑established body of research demonstrates that strategic partnerships enhance competitive advantage, particularly in emerging economies where markets are inefficient and formal institutions are weak (Olutimehin, 2024). According to the power‑of‑relationships thesis, “in Africa, the operating system isn’t always logical, it’s relational” (Wechoemang, 2025: 1). Formality only works after informality clears the path, meaning that relational equity and social proof cannot be purchased or pitched - they must be earned through embeddedness .

Yet much of what's been written zeroes in on official partnerships, shared business efforts, or company groupings while skipping over the personal roots -like deep trust between people. Few studies look closely at long-standing friendships, bonds stronger than casual knowing, and how these shape the way things get done behind the scenes. The existing studies of international joint ventures in Africa (e.g., studies of IJV partner origin in Ghana) find that the origin of a partner influences strategic choices such as an efficiency‑oriented versus innovation‑oriented strategy , but they do not differentiate between institutional partners and personal friends.

2.2 Social Capital, Friendship Ties and Informal Governance

Social capital theory provides a useful lens for understanding the value of relationships. Social capital refers to the resources embedded in a firm’s network of relationships, including trust, norms of reciprocity, and information channels. For multinational enterprises, “firms operating in global markets rarely have adequate resources to compete effectively; they access needed resources through formal and informal relationships with other firms” .

The literature further distinguishes between internal network configuration (density, hierarchy) and external ties. However, almost all studies in this tradition treat "social ties" as aggregated network properties (e.g., number of contacts, frequency of interaction). What is largely absent is a micro‑level analysis of how a single, intensely loyal friendship between founders affects the firm’s governance structure, risk appetite, strategic speed and succession planning. In Africa, the role of social ties in performance has been identified in the context of small‑ and medium‑sized enterprises (Aluko et al., 2019; Udry and Conley, 2004), but there is a noticeable scarcity of research on large, listed corporations where such ties persist into the bluechip phase. This gap is especially striking because business groups in many emerging economies are often built around family or ethnic ties, yet the study of “friendship” as a distinct governance vehicle remains underdeveloped.

2.3 Institutional Voids and the Network‑Based Entry Mode

One of the most influential concepts in emerging‑market strategy is that of “institutional voids” which is the absence of market intermediaries, contract‑enforcing mechanisms, and regulatory transparency. A recent stream of research argues that firms entering African markets often overcome voids by entering as a collective, relying on “bridging networks” (i.e., extending an existing loose network to facilitate entry). This network‑ecosystem approach explains why business groups and loose alliances are so prevalent in sub‑Saharan Africa (Turcan & Dholakia, 2021) . Moreover, “network entry facilitates market access speed and may allow for local ties to remain undeveloped or be a first step in building in‑country networks”.

What the network entry literature does not address is that many of the most successful bridging networks are not ephemeral, formal alliances but rather long‑standing personal friendships. Access Bank’s acquisition spree across Southern and East Africa (South Africa, Kenya, Mozambique and Zambia) was not driven by a consultant‑designed alliance strategy; it was driven by the speed and decisiveness that came from two friends who trusted each other completely. Similarly, Oando’s decision to partner with Helios Investment Partners to sell 49 % of its mid‑stream subsidiary was made credible by the fact that the Oando founders’ personal relationships with Helios’s principals were built years before the transaction.

2.4 Bluechip Transitions in Africa

The term “bluechip” is generally defined as a stock of a corporation that is huge, well‑funded, profitable under any circumstances, and with a market capitalisation typically exceeding $10 billion (in global markets) . In the Nigerian context, the bluechip threshold is often expressed as a market cap above N1 trillion, a level that Access Bank, MTN Nigeria, Dangote Cement and Seplat Energy have all crossed. The attraction of bluechip listings in emerging stock exchanges is a major policy initiative, yet many local bluechip firms are the result of foreign MNE local partner joint ventures (Bruce, 2015) . Very few studies have investigated how indigenous African firms achieve bluechip status primarily through endogenous relationships. Those that do exist (e.g., studies of Dangote Industries’ growth) focus on the role of infrastructure investment and vertical integration, not on the founders’ relational capital.

2.5 Synthesis and Research Gap

After synthesising these literatures, the research gap becomes clear: there is no dedicated study that examines how “loyal friend networks” function as governance catalysts for bluechip status, especially when those friends share a broader vision of African liberation. The Access Bank and Oando cases provide vivid illustrations, but so far these remain anecdotal. The present article fills this gap by developing a theoretical framework that integrates social capital theory with the institutional voids and network entry perspectives, and testing it through systematic comparative case analysis.

Theoretical Framework

In this narrative methodology propose a framework called Vision‑Aligned Relational Governance (VARG). One piece holds it up. Then another fits beside. A third locks everything into place

1. Friendship that lasts a long time shapes how close people are. How often they talk matters just as much as how far back they go. Ties formed before any business started tend to run deeper. Length of connection often shows up in small, repeated moments. What counts is not only years but shared history showing through actions.

2. Freedom shared means goals shaped by Africa's own economy first. When company aims tie into stronger unity across African nations, that counts too. Less need for outside money becomes part of the plan, slowly built in. A firm’s direction matters most when it lines up with these shifts. Ownership stays local because of choices made day after day.

3. Decisions flow through trust, sidestepping red tape. Speed picks up when rules fade into the background. Acquiring assets becomes quicker, almost fluid. Bolder bets emerge without needing layers of approval. Resources shift where they’re needed, quietly, without fanfare. Flexibility grows when structure loosens its grip.

Out past ties shaping common goals might lift company results beyond what strict plans alone could do. When trust links mix with aligned aims, something extra shows up in growth numbers. That boost comes not just from official blueprints on paper. It appears where relationships meet direction. What counts here isn’t policy by itself. The real effect hides in how people work together behind the scenes. Not every gain traces back to top-down design. Some of it grows quietly from mutual understanding. Performance climbs when connection feeds purpose. Numbers rise slower without that blend. Shared sight plus deep bonds create more than either does alone.

3. Conceptual Framework

The study introduces Visionary Friendship Governance Theory (VFGT), structured as:

3.1. Governance Index Calculation Model

3.1.1 Visionary Friendship Index (VFI)

VFI. = BT+ET+CS+SD+NS

5

Where:

BT = Board Tenure overlap score

ET = Executive tenure stability

CS = CEO - CFO continuity score

SD = Strategic decision co-occurrence density

NS = Network stability score

3.1.2 Relational Governance Intensity (RGI)

RGI = αVFI+βEC+γCI

Where:

EC = Executive cohesion

CI = Communication intensity

α, β, γ = weighting coefficients (0–1)

3.1.3 Decision Velocity (DV)

DV= 1 x Sexpansion

Tdecision

Where:

Tdecision = average decision time

Sexpansion = strategic expansion scale factor

3.1.4 Corporate Performance Index (CPI)

CPI= ROA+ROE+RG+M+I

5

Where:

RG = Revenue growth

M = Market capitalization growth

I = Internationalization index

This would be worked on during the next article presentation as we build the research further.

4. Methodology

4.1 Research Design

The study adopts a comparative qualitative case study design supported by interpretive secondary quantitative synthesis. This approach allows for deep contextual analysis of governance mechanisms across two African multinational corporations operating in distinct industries.

The design is appropriate because relational governance is a context-dependent phenomenon that cannot be fully captured through cross-sectional surveys alone. Case study logic enables examination of embedded governance structures within real organizational settings.

4.2 Case Selection

Access Bank and Oando Group were purposively selected on the basis of three criteria:

- l Blue‑chip status: Both firms have achieved a market capitalisation in excess of N1 trillion (Access Holdings ~₦1.38 trillion in 2025; Oando ~₦612–832 billion depending on valuation period, with peak above N1 trillion). Access bank is widely described as one of Africa’s bluechip financial institutions .

- l Founder friendship longevity: In both cases, the controlling founders are known to have maintained a close personal relationship for 20+ years before the major scaling phase.

- l Pan‑African/liberation vision: Both firms explicitly invoke continent‑wide transformation as part of their corporate mission.

4.3 Data Sources

We triangulated multiple sources:

- l Market cap, income, and earnings before tax come from NGX filings. Data spans 2020 to 2026. Sources include StockAnalysis, Trading Economics, plus updates from finance-focused outlets. Numbers are pulled directly where available.

- l Company updates come through official statements about buying other firms, merging with them, raising money, or teaming up for long-term plans.

- l From fifty-six confirmed news pieces came a look into past events. Annual general meetings showed up across these records too. Interviews already made public added founder voices alongside director remarks now and then. Coverage stretched through time, pulling details from media corners less visited. Each piece helped shape what stood clear after checking sources twice.

- l Governance documents: Board compositions, interlocking directorates and committee structures, where available.

4.4 Analytical Strategy

The analysis followed three steps. Step one built a sequence of major choices - like buying companies or entering fresh markets - for every situation. Not long after, it became clear where close bonds between founders might have shaped moves that demanded deep confidence, quick action, or bending standard rules. Then came spotting similarities across examples, watching how personal ties quietly helped reach

top-tier success. Patterns showed up when trust ran deeper than policy.

5. Findings

5.1 Case A: Access Bank (Aig‑Imoukhuede and Wigwe)

5.1.1 Friendship Genesis and Shared Vision

Back in the early nineties, Aigboje Aig-Imoukhuede crossed paths with Herbert Wigwe while working at GTB in Lagos - no campus reunion, just office corridors. That bank opened its doors in 1990, becoming the shared ground where both men shaped what came next. Born September 24, 1966, Aig-Imoukhuede walked through law school at the University of Benin, grabbing an LLB by 1986, later adding an MBA from the very same institution. Wigwe, entering the world August 15 that same year, took a different path - one lined with numbers - at UNN, studying accounting before finishing up in 1987.

Inside GTB’s fast-moving world, a common hunger took root between them. From Aig-Imoukhuede’s own account, each wanted one thing - ownership of a bank. That aim stretched past individual success; by the early 2000s, he sensed an opening for something bold across Africa, later admitting he dreaded standing idle while change moved without him. Their deep bond and matching vision gave space to walk away from leading positions at GTB. In 2002, that leap led straight to buying Access Bank when it was barely holding on. Their subsequent expansion strategy reflected a focused execution of a shared vision.

5.1.2 The Diamond Bank Acquisition: A Milestone in Access Bank’s Trajectory

The acquisition of Diamond Bank in 2019 was a landmark transaction that propelled Access Bank into a new league. Announced in December 2018, the deal valued Diamond Bank at N72.5 billion (approximately $235 million), representing a 260% premium to the target’s market price at the time. The offer comprised N1.00 in cash per share plus two new Access Bank shares for every seven Diamond Bank shares held.

The acquisition positioned Access Bank as Africa’s largest bank by customer base, bringing together 29 million customers across 12 countries and three continents. As Herbert Wigwe stated at the time, the merger would “create a leading Tier 1 Nigerian bank and the largest bank in Africa by number of customers.” The transaction received all necessary approvals, including the Central Bank of Nigeria’s “no objection” in January 2019 and final shareholder approval in March 2019 and was formally completed on April 1st, 2019, when Diamond Bank was fully merged into Access Bank and ceased to exist as a legal entity.

Beyond the transaction itself, the integration was a strategic tour de force. Between 2019 and 2021, Access Bank realized ₦153.9 billion in expected cost savings and loss recoveries from the merger, with ₦59.9 billion recorded by the end of 2019 alone. Within one year of completion, the group delivered gross earnings of N209.8 billion, a 31% increase year‑on‑year. The integration also involved a full core‑banking platform consolidation to ensure long‑term scalability.

The Diamond Bank transaction was a defining example of friend‑led, vision‑aligned governance. While the deal’s scale required board oversight, the decision to pursue such an ambitious merger such as acquiring a bank that had struggled since 2016 to bolster its capital following loan losses that was championed by the two founders, who brought the proposal to the board with unified authority. Wigwe’s subsequent public explanation of the deal “to acquire a bank with 17 million retail customers and the most viable mobile payment platform” which reflected the shared strategic worldview that Aig‑Imoukhuede and he had developed over decades . The CBN was also known to have “midwifed the acquisition in a bid to further consolidate the banking industry,” requiring the trust and speed that only a unified founding team could provide.

5.1.3 Broader Pan‑African Expansion Through Trust‑Based Governance

The Diamond Bank acquisition was part of a broader growth strategy. From 2010 to 2025, Access Bank moved into over 25 nations - South Africa, Kenya, Mozambique, Zambia among them. Yet it was the deep trust between Aig-Imoukhuede and Wigwe, their matching vision of achievement, that made swift approval of takeovers possible across official channels. Because they operated on such alignment, red tape thinned out; timing-heavy chances got taken without delay.

5.1.4 Financial Path Toward Bluechip Recognition

Back in 2002, Access Bank held roughly ₦3.8 billion in assets, placing it at number 65 among Nigeria’s 89 banks. Its climb began slowly but gained speed over time. Come 2019 - just after merging with Diamond Bank - earnings jumped by 26 percent annually, reaching ₦667 billion. Growth didn’t stall; instead, it accelerated sharply. By 2024, those earnings swelled again, up 88 percent yearly, hitting ₦4.878 trillion. Shareholders then backed payouts totaling N125.3 billion. Numbers like these tell the real story behind its rise. In the 2025 financial year, Access Holdings’ profit‑before‑tax crossed the N1 trillion mark for the first time, cementing its bluechip status. Table 2 summarises key performance milestones, including the Diamond Bank acquisition.

5.1.5 The Role of the AfriCaribbean Vision

A distinctive feature of Access Bank’s recent strategic orientation is the explicit AfriCaribbean focus. At the AfriCaribbean Trade and Investment Forum (ACTIF) 2025, Aig‑Imoukhuede personally led the bank’s engagement, where Access Bank announced an expanded strategic alliance with Afreximbank to “boost trade finance, capacity building, and tailored financial solutions for Caribbean markets” . This vision shapes capital allocation (e.g., establishing Caribbean subsidiaries) and signals an identity anchored in African liberation, intended to attract diaspora capital and loyalty.

5.2 Case B: Oando Group (Wale Tinubu and Omamofe Boyo)

5.2.1 Friendship Origins and Shared Energy‑Independence Vision

Wale Tinubu and Omamofe Boyo grew up together in Lagos and attended the same secondary school before studying law at the University of Lagos. Their friendship dates back to childhood. In the 1990s, they co‑founded a small oil‑trading firm that eventually became Oando PLC. As the company grew into exploration, production and gas distribution, the two friends maintained a partnership in which Tinubu served as Group Chief Executive and Boyo as Deputy Group Chief Executive.

Their shared vision centers on energy independence for Africa. Oando’s strategy has consistently emphasized building indigenous capacity to explore, produce and distribute oil and gas without surrendering strategic control to international majors. This liberation orientation is sometimes framed as the “post‑colonial imperative” to recapture value that historically flowed out of the continent.

5.2.2 Strategic Partnerships with Helios Investment Partners

A signature moment in Oando’s trajectory was the 2016 mid‑stream partnership with Helios Investment Partners. Oando signed a $115.8 million agreement whereby Helios would acquire 49 % of the voting rights in Oando Gas and Power (OGP). According to the Group Chief Executive, “This strategic alliance will firmly leverage our local knowledge and expertise alongside Helios’ strong financial capabilities” . While this is formally an equity partnership, its relational basis is crucial: the principals at Helios were known to the Oando founders from previous industry interactions, and the deal was negotiated quickly on the basis of mutual trust rather than prolonged legal wrangling. After completion, Oando retained 49 % of voting rights (the remaining 2 % was held by a local entity) .

5.2.3 Financial Trajectory and Blue‑chip Entry

Oando’s stock market performance has been volatile but spectacular. Between 2023 and 2024, the share price rose dramatically, pushing the company into the N1 trillion market‑cap club. One report noted: “Oando has joined the exclusive list of companies with a market capitalisation above N1 trillion, being the second oil and gas company in the category, the other being Seplat Energy Plc”. In 2025, the stock recorded the single‑largest price gain on the NGX on a given day, closing at N51.70, reflecting sustained investor confidence . Table 3 presents key performance indicators.

5.2.4 How Friendship Mediated the Helios Alliance

The conventional interpretation of the Helios‑Oando alliance is a simple JV transaction. However, the transaction exhibited characteristics of friendship‑mediated governance: it was negotiated at the top‑management level without a protracted bidding process, and the governance of the joint venture was explicitly designed to preserve Oando’s operational autonomy (Oando retained 49 %). Tinubu described it as “leveraging our local knowledge alongside Helios’s strong financial capabilities,” a formulation that assumes the two sides’ principals can work together without friction - an assumption rooted in prior personal trust.

5.3 Cross‑Case Comparison

A cross‑case comparison reveals three common patterns of friend‑network governance:

1. Speed of high‑stakes decisions: In both Access and Oando, major strategic moves (acquisitions, continent‑wide expansion, equity partnerships) were executed more quickly than peer institutions.

2. Risk‑taking aligned with a liberation vision: Neither firm adopted a cautious, incremental internationalization path. They entered high‑potential but challenging markets (e.g., Access into Mozambique and the Caribbean; Oando into capital‑intensive gas infrastructure) because the founders’ mutual trust reduced perceived risk.

3. Long time horizon: Because the friendships predate the firms, founders do not face the typical short‑term pressure of a CEO‑board relationship. They can thus invest in long‑term, vision‑consistent projects, even when these projects take years to pay off.

6. Discussion

6.1 Theoretical Contributions

This article makes three main contributions to theory.

First, it introduces the construct of vision‑aligned relational governance (VARG), which specifies how friendship‑based ties among founders can function as a firm‑specific advantage, particularly in navigating institutional voids. Existing institutional‑voids literature has emphasised the role of market intermediaries and cross‑sector alliances (Turcan & Dholakia, 2021). It has not specified that the most effective bridging networks are often ones built on long‑standing personal trust. This study shows that VARG reduces two major transaction costs: the cost of monitoring (friends trust each other, so fewer hierarchical controls are needed) and the cost of decision delay (trust enables speed).

Second, the article bridges the social‑capital literature and strategic management in emerging markets. Prior social‑capital studies in Africa have focused on small firms or aggregative network measures (Aluko et al., 2019). By focusing on large, bluechip corporations and tracing the micro‑processes through which friendship influences strategic decisions, this study extends social‑capital theory to the upper echelons of emerging‑market corporate governance.

Third, the article contributes to the concept of entrepreneurial vision. The “African liberation” narrative, whether expressed as “bridge Africa‑Caribbean” (Access) or “energy independence” (Oando) is not merely decorative. It functions as a motivational anchor that keeps the founding partners aligned when facing setbacks. Because their vision matched, these companies skipped quick profits to back big changes across entire regions. What happened shows success in developing markets depends less on spending choices and more on shared stories and who they believe they are.

6.2 Practical Implications

Policymakers need to see beyond just rules on paper - trust among founders matters too. While new guidelines roll out across Africa, like Nigeria’s 2023 update, old loyalties remain untouched. Board reshuffles mean little if personal bonds steer decisions behind closed doors. Reform talks skip over coffee chats that shape company fates. Stronger oversight must make space for how people really connect, not just how they’re supposed to act. What happens between meetings often counts more than what shows up in minutes. However, for many indigenous firms, the friendship is the governance mechanism. Any regulatory reform that destroys the relational capital of founders (e.g., by requiring that CEOs and board chairs be separate even when they are trusted partners) could be counter‑productive.

For entrepreneurs, the key lesson is that friendship is not a liability (“bringing friends into business”) but can be a strategic asset if it is accompanied by a shared, transcendent vision. The Access‑Oando experience suggests that a friendship that survives early‑stage survival struggles can become a long‑term governance engine.

For investors, the implication is that due‑diligence frameworks should explicitly assess the quality and duration of personal relationships among top management teams. A founding team that has known each other for 20 years and has a track record of making collective strategic decisions is likely to be more resilient in turbulent times than a team assembled for a short‑term financial project. This kind of relational capital is difficult to replicate and can be a reliable predictor of bluechip achievement.

6.3 Limitations

This study has several limitations for now. First, it relies on publicly available data and media reports. Although the triangulation of sources increases confidence, the lack of access to board meeting minutes and private correspondence limits the ability to definitively prove causation. Second, the case selection method may be subject to selection bias: both Access and Oando are success stories. The role of friendship networks in firms that failed to achieve bluechip status may be different, and that counter‑factual is missing. Third, the concept of “African liberation vision” is not straight forward to measure; the article adopted a qualitative approach, but future research could develop quantifiable indicators and elaborate further on the conceptual framework and methodology before publishing on acadmeic journal.

A related limitation concerns the financial crisis of 2024 2026, which affected both firms. The analysis does not disentangle the effect of the macro environment (currency depreciation, inflation) from the effect of relational governance.

6.4 Future Research Directions

Several directions for further research emerge. First, a quantitative study could operationalise the VARG framework, collecting primary data on founder‑friendship duration, visionary statements, and corporate performance indicators across a larger sample of African publicly listed firms. Second, qualitative comparative analysis (QCA) could test necessary and sufficient conditions for friend‑network governance to produce bluechip outcomes. Third, ethnographies of founder boards (where researchers observe decision‑making) could directly trace how informal interactions affect formal votes. Fourth, longitudinal studies of the post‑founder phase (succession from the founding friends) would shed light on whether bluechip resilience can survive the transition to professional managers.

Finally, comparative research across emerging markets (Latin America, South‑East Asia) would help to determine whether the VARG phenomenon is particularly African (i.e., shaped by colonial‑era institutional voids) or more general.

7. Conclusion

This article set out to answer a simple but neglected question: do loyal friendships among founders who share a vision of African liberation contribute to building bluechip corporations? Through a detailed comparative analysis of Access Bank and Oando, this study has shown that long‑standing, trust‑based friend networks operate as informal governance mechanisms that accelerate strategic decisions, enable riskier continental expansion, align long‑term capital allocation with a transcendent vision and ultimately help firms cross the bluechip threshold. While no single case study can definitively prove causality, the evidence marshalled here strongly suggests that the friendship between Aig‑Imoukhuede and Wigwe, and that between Tinubu and Boyo, was not incidental to their firms’ success but central to it.

Significant research gaps remain - exactly as the literature review indicated - but this article has begun the work of filling them. For theory, it has offered a new construct (VARG) and demonstrated its applicability. For practice, it has highlighted the strategic value of loyal, vision‑aligned friendships in emerging‑market governance. For Africa, where the discourse on economic development often focuses on macro‑policy and infrastructure, the message is that person‑to‑person trust is built over decades and motivated by a shared vision of liberation which can be as powerful a driver of prosperity as any structural adjustment programme.

MORE READ:

- Lagos International Financial Centre: Nigeria’s New Economic Blueprint

- How Corporate Governance Drives the Survival and Growth of Emerging Enterprises

- Why Strong Corporate Governance Is the Secret to African Business Survival

- Digital Governance in Nigeria, Why Corporate Boards Must Treat AI, Cybersecurity and Data Ethics as Fiduciary Duties

Contact: report@probitasreport.com

Stay informed and ahead of the curve! Follow The Probitas Report on WhatsApp for real-time updates, breaking news, and exclusive content especially on integrity in business and financial fraud reporting. Don’t miss any headlines, connect with us on social media @probitasreport and visit www.probitasreport.com WhatsApp Only: +234 902 148 8737

[©2026 ProbitasReport - All Rights Reserved. Reproduction or redistribution requires explicit permission.]

What's Your Reaction?