Zenith Bank Q1 2026 Results: Financial Analysis, Profitability, and Key Performance Insights

A detailed financial analysis of Zenith Bank PLC Q1 2026 results, highlighting profitability, efficiency, asset quality, liquidity, and overall financial health.

In a period marked by economic uncertainty and tightening financial conditions, Zenith Bank PLC has delivered a performance that reinforces its reputation as one of Nigeria’s most resilient financial institutions. Its Q1 2026 results reveal a compelling mix of strong profitability, disciplined cost management, and robust capital strength. However, beneath these impressive numbers lie critical signals such as rising credit costs and moderating profit growth that demand closer scrutiny. This analysis unpacks the key drivers of performance, highlights emerging risks, and provides a clear view of what lies ahead for the bank and the broader Nigerian banking sector.

A summary and in-depth financial analysis of Zenith Bank PLC's unaudited interim financial statements for the period ended 31 March 2026, based on the document provided.

Executive Summary

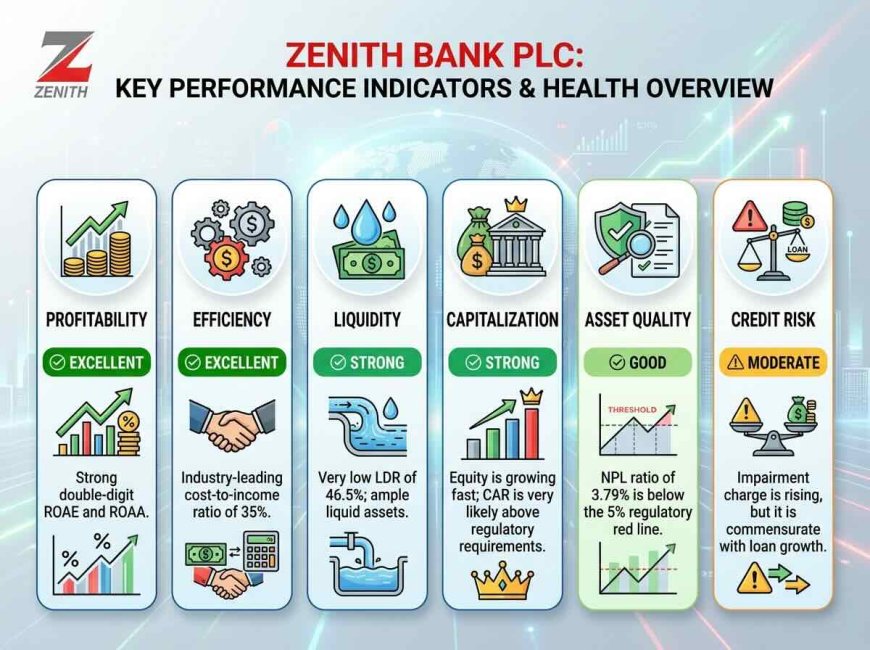

Zenith Bank PLC has reported a solid financial performance for the first quarter of 2026. The Group shows strong profitability, robust asset growth, and a very healthy capital position. Key challenges include a significant increase in the impairment charge for credit losses and pressure from operating expenses, though these are largely in line with asset growth. The bank remains highly efficient, profitable, and well-capitalized, with a non-performing loan (NPL) ratio that is well within the regulatory threshold.

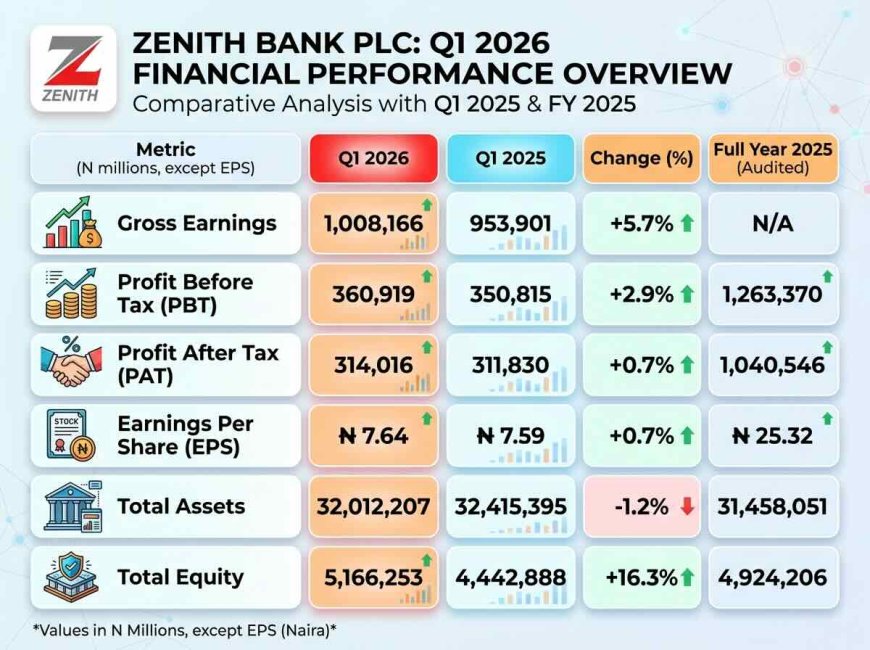

1. Financial Performance Summary (Group)

Analysis: The bank achieved modest year-on-year growth in profitability for Q1 2026. While PBT and PAT increased by approximately 3% and 0.7% respectively, this growth rate slowed compared to the exceptional performance seen in the full year 2025. Total assets contracted slightly by 1.2% from March 2025 but grew 1.8% from December 2025. The most striking improvement is in total equity, which surged by 16.3% year-on-year, indicating strong internal capital generation.

2. Key Financial Ratios & Analysis

A. Profitability Ratios

-

Return on Average Equity (ROAE): (Annualized PAT / Average Equity)

-

Calculation: (314,016 * 4) / ((5,166,253 + 4,924,206)/2) = 1,256,064 / 5,045,229.5 = ~24.9%

-

Analysis: Zenith Bank remains exceptionally profitable for its shareholders, generating a near 25% return on equity. This is a very strong figure for a commercial bank.

-

-

Return on Average Assets (ROAA): (Annualized PAT / Average Assets)

-

Calculation: (314,016 * 4) / ((32,012,207 + 31,458,051)/2) = 1,256,064 / 31,735,129 = ~3.96%

-

Analysis: An ROAA of nearly 4% is excellent and indicates the bank is very effective at using its asset base to generate profits.

-

-

Net Interest Margin (NIM): (Net Interest Income / Average Interest-Earning Assets) - Approximated

-

Net Interest Income (Q1) = N869.1bn (Income) - N235.0bn (Expense) = N634.1bn

-

Annualized NIM = (634.1 * 4) / 32,012,207 = ~7.9%

-

Analysis: The NIM is healthy, showing the bank earns a strong spread between the interest it receives on loans/investments and the interest it pays on deposits/borrowings.

-

B. Efficiency Ratio

-

Cost-to-Income Ratio: (Operating Expenses / Gross Earnings)

-

Calculation: 354,657 / 1,008,166 = 35.2%

-

Analysis: This is an outstanding efficiency ratio. It means the bank spends only about 35 kobo to generate every one Naira of income. A ratio below 50% is generally considered good; below 40% is excellent. Zenith Bank is highly efficient.

-

C. Liquidity & Capital Adequacy

-

Loan-to-Deposit Ratio (LDR): (Net Loans / Customer Deposits)

-

Calculation: 11,382,174 / 24,473,674 = 46.5%

-

Analysis: This ratio is very conservative and well below the Central Bank of Nigeria's (CBN) regulatory minimum (often >65%). It indicates the bank has significant liquidity and is not overly reliant on deposits to fund its loan book. It has ample room to grow its lending portfolio.

-

-

Capital Adequacy Ratio (CAR) - Estimated: The bank does not provide the risk-weighted assets (RWA) in this report. However, total equity of N5.17 trillion against total assets of N32.0 trillion gives a crude leverage ratio of ~16%. Given that RWA are typically a portion of total assets, Zenith Bank's CAR is almost certainly well above the CBN's prudential requirement of 15% (for a bank with a national banking license).

-

Cash & Liquidity: The bank holds N6.75 trillion in cash and central bank balances. Of this, N5.89 trillion is the mandatory cash reserve requirement (CRR), functioning as a restricted asset. Excluding CRR, liquid assets (T-bills, due from other banks, unencumbered cash) remain substantial, supporting strong liquidity.

D. Asset Quality & Risk (NPL Ratio & Coverage)

This is a critical area for any bank. The report uses IFRS 9 Expected Credit Loss (ECL) model.

-

Non-Performing Loan (NPL) Ratio:

-

Gross Loans: N12,039,373 million

-

Credit-Impaired Loans (Stage 3 - Lifetime ECL): N456,292 million (from Note 27)

-

NPL Ratio: 456,292 / 12,039,373 = 3.79%

-

Analysis: The NPL ratio of 3.79% is excellent and well below the CBN's maximum threshold of 5%. It has also improved significantly from the FY 2025 NPL ratio (based on impaired loans of N422,408 billion: 422,408 / 11,063,866 = 3.82%). This indicates strong underwriting standards and effective credit risk management.

-

-

NPL Coverage Ratio: (Total ECL allowance for Stage 3 loans / Gross Stage 3 Loans)

-

ECL Allowance for Stage 3 Loans: N337,996 million (from Note 27)

-

Coverage Ratio: 337,996 / 456,292 = 74.1%

-

Analysis: A coverage ratio of 74% is prudent. The bank has set aside over 74 kobo for every one Naira of non-performing loan. This provides a strong buffer against potential future write-offs.

-

-

Impairment Charge: The charge for credit losses increased by 16.6% (from N49.4bn to N57.6bn) year-on-year. While a negative trend, this is likely a reflection of the growing loan book (gross loans grew 8.6% year-on-year) rather than a systemic deterioration in asset quality, which the low NPL ratio confirms.

3. Overall Health & Verdict

Based on the Q1 2026 financial statements, Zenith Bank PLC is in a very strong and healthy financial position.

Strengths:

-

Superior Efficiency: The 35% cost-to-income ratio is a standout metric, showcasing world-class operational management.

-

High Profitability: Sustained high returns for shareholders.

-

Excellent Asset Quality: NPL is under control and well-provided for.

-

Strong Capital Base: Provides a significant cushion against unexpected losses and supports future growth.

Weaknesses/Areas to Watch:

-

Slowing Profit Growth: Profit growth was modest compared to the previous year. Investors will want to see if this is a one-off or a trend.

-

Rising Credit Costs: The increase in the impairment charge needs to be monitored to ensure it doesn't outpace income growth.

-

High CRR (External Factor): A significant portion of liquid assets (N5.89 trillion) is locked in mandatory CRR with the CBN. While a fact of operating in Nigeria, this restricts the bank's ability to deploy these funds for higher-yielding activities.

Conclusion: Zenith Bank remains a barometer of the Nigerian banking industry. Its Q1 2026 results demonstrate a highly efficient, profitable, and well-capitalized institution with strong risk management practices. The bank is in excellent health and well-positioned for the remainder of the 2026 financial year.

MORE READ:

- Lagos International Financial Centre: Nigeria’s New Economic Blueprint

- How Corporate Governance Drives the Survival and Growth of Emerging Enterprises

- Why Strong Corporate Governance Is the Secret to African Business Survival

- Digital Governance in Nigeria, Why Corporate Boards Must Treat AI, Cybersecurity and Data Ethics as Fiduciary Duties

Contact: report@probitasreport.com

Stay informed and ahead of the curve! Follow The Probitas Report on WhatsApp for real-time updates, breaking news, and exclusive content especially on integrity in business and financial fraud reporting. Don’t miss any headlines, connect with us on social media @probitasreport and visit www.probitasreport.com WhatsApp Only: +234 902 148 8737

[©2026 ProbitasReport - All Rights Reserved. Reproduction or redistribution requires explicit permission.]

What's Your Reaction?