The Hidden Strain: How Loan Defaults Are Stifling Growth for Nigerian Businesses and Households

Explore how rising loan defaults are impacting Nigerian businesses and households, hindering economic growth, and what strategies can help mitigate financial risks.

We’ve all been there. Money is tight, an opportunity arises, or an emergency hits. The logical step? Maybe a loan. For countless Nigerian businesses and households, credit isn't just a financial tool; it's a lifeline. It’s the seed capital for a market stall, the invoice discounting that keeps an SME afloat, or the school fees that secure a child's future.

But what happens when that lifeline snaps? When loans stop performing, the ripple effects are far more profound than a line item on a bank’s balance sheet. The rising challenge of non-performing loans (NPLs) is a silent crisis, draining our economy, stunting business growth, and plunging families into distress. This isn't just a story about banks losing money; it's about the very real human and institutional cost of loan defaults in Nigeria.

In early 2025, the total stock of NPLs surged past a staggering ₦1.57 trillion, painting a clear picture of a system under stress.

What Exactly Are Non-Performing Loans (NPLs)?

Let's demystify the jargon. A Non-Performing Loan (NPL) is a financial term used to describe a loan in which the borrower has failed to make scheduled payments of principal or interest for a specified period, typically 90 days or more. This classification indicates that the loan is in default or close to default, signaling a heightened risk of non-repayment. NPLs are a significant concern for financial institutions as they can adversely affect profitability and capital adequacy. The accumulation of NPLs within a banking sector may lead to tighter credit conditions, higher interest rates, and reduced lending activities, thereby impacting economic growth.

In the context of consumer loans, a loan is considered non-performing if payments are overdue by 180 days. The classification of a loan as non-performing is subject to regulatory standards and may vary across jurisdictions. For instance, the European Central Bank defines an NPL as a loan where there are indications that the borrower is unlikely to repay, or if more than 90 days have passed without payment. Effective management and resolution of NPLs are crucial for maintaining the stability of financial systems and ensuring continued access to credit for borrowers. Whilst a certain level of NPLs is normal in any banking system, Nigeria's figures have been a persistent cause for concern.

The Domino Effect: How One Default Hurts Everyone

The domino effect of a loan default shows that the cost is never isolated, as it sets off a chain reaction that eventually touches every part of the economy. For banks, a default directly impacts profitability, as capital that should be earning interest becomes tied up in bad debt. To compensate for these losses and meet regulatory requirements, banks

are forced to tighten their purse strings, becoming more risk-averse, lending less, and charging higher interest rates to everyone else to cover the shortfall from defaulters; this is the first domino to fall. For honest borrowers, the impact is immediately felt, as the cost of loan defaults is socialized: diligent business owners who repay on time now face higher borrowing costs, and access to affordable credit shrinks, punishing the responsible for the actions of others. For the national economy, a credit-starved environment leads to stagnation, with SMEs unable to expand, corporations hesitant to invest in new projects, and job creation stalled. Furthermore, a high level of non-performing loans deters foreign investors, who perceive it as a sign of financial instability.

“To protect tomorrow’s economy, we must restore today’s confidence in credit”

… Dr Ohio O. Ojeagbase

The Crushing Weight on Nigerian SMEs

If there is one sector that bears the brunt of this crisis, it is small and medium enterprises, which serve as the engine of our economy yet remain the most vulnerable. Recent data is alarming: in the second quarter of 2025, small businesses recorded the sharpest drop in loan performance, with a default index falling to -7.2. The challenges faced by SMEs are immense, as they often lack the extensive collateral of larger corporations and are more exposed to economic shocks such as inflation and currency fluctuations. When an SME defaults, it is not just a statistic; it can result in stunted growth due to the inability to secure new funding for expansion, job losses when the business closes and employees lose their livelihoods, and the suffocation of innovation as great ideas never see the light of day because of a lack of capital.

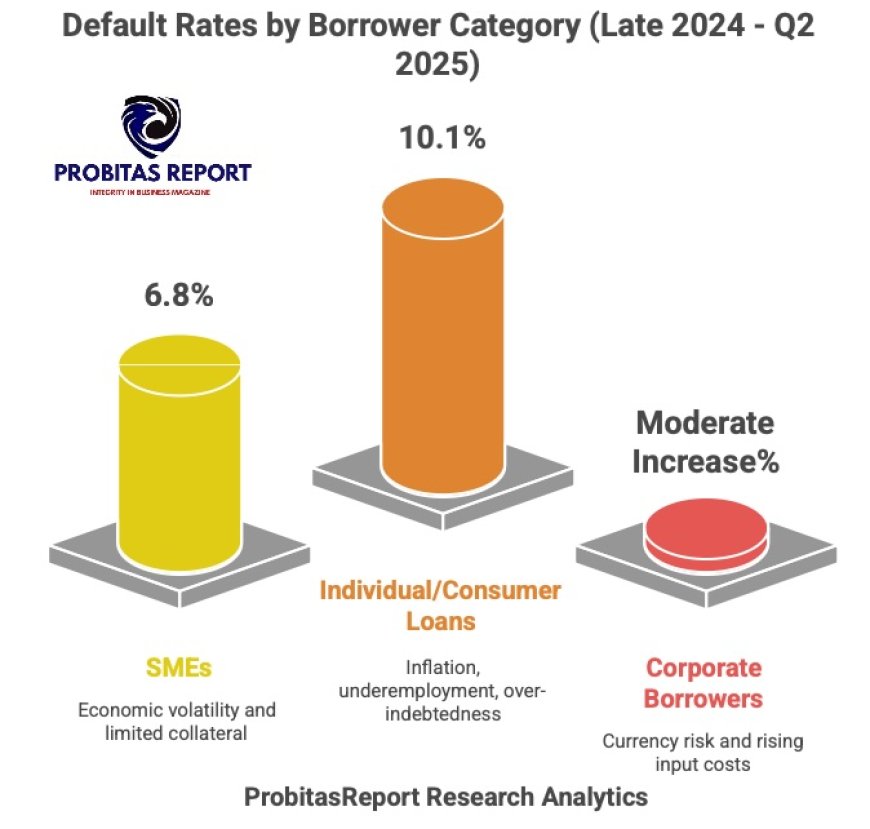

The table below breaks down the recent spike in default rates across different borrower categories, highlighting the acute pressure on SMEs:

|

Borrower Category |

Default Rate (Late 2024 - Q2 2025) |

Key Challenge |

|

Small & Medium Enterprises (SMEs) |

6.8% - Sharp Increase |

Economic volatility, limited collateral |

|

Corporate Borrowers |

Moderate Increase |

Currency risk, rising input costs |

|

Individual/Consumer Loans |

10.1% (Unsecured Loans) |

Inflation, underemployment, over-indebtedness |

Data compiled from CBN reports and Nairametrics analysis.

The Human Cost: Household Debt in Nigeria

Beyond the boardrooms, the crisis seeps into our homes. Household debt in Nigeria is becoming an increasingly heavy burden. With inflation squeezing disposable income, many families turn to credit to make ends meet. When they can't keep up, the consequences are devastating.

The immediate effects are financial: harassing phone calls from collectors, the threat of asset repossession (like that car used for ride-sharing), and a damaged credit history that slams the door on future financial help. But the deeper cost is human. A recent study explored the mental health impacts of debt and default, finding that the constant anxiety and stress can be crushing. The fear, the shame, and the feeling of being trapped take a severe psychological toll, affecting health, relationships, and overall well-being. Loan repayment issues transform from a financial problem into a full-blown life crisis.

Debt Recovery Nigeria: Not Punitive, But Essential

The term "debt recovery" often conjures images of aggressive confrontations. This needs to change. Effective debt recovery in Nigeria is not about punishment; it's about responsibility and system preservation. A robust and fair recovery process is a necessary pillar of financial security. It ensures that capital continues to circulate, that lenders can remain in business to serve other customers, and that responsible borrowers aren’t unfairly penalized. The goal should be to create a system where recovery is efficient, transparent, and ethical, protecting the rights of both lenders and borrowers.

Building a New Credit Culture Nigeria

Building a new credit culture in Nigeria requires a collective effort from all sides to break the cycle of loan defaults. Borrowers, both individuals and businesses, must embrace borrowing as a serious commitment by conducting due diligence, maintaining a clear repayment plan, and communicating proactively with their lenders if they encounter financial difficulties, as honoring debts is an ethical responsibility that strengthens their financial reputation. Lenders, including banks and FinTechs, should practice responsible lending by conducting proper affordability checks, educating customers on loan terms, and offering support and restructuring options before a loan becomes non-performing. Regulators, meanwhile, need to strengthen infrastructure by expanding the coverage and effectiveness of credit bureaus to ensure that credit histories, whether good or bad, follow individuals, while streamlining the legal framework for contract enforcement to make debt recovery faster and more predictable.

A Path Forward: From Drain to Gain

The tide of non-performing loans does not have to be a permanent feature of our economic landscape. By reframing the conversation from one of blame to one of shared responsibility, we can begin to address and reduce this drain. Debt should be seen not as a trap, but as a tool; repayment should be viewed not as a burden, but as a cornerstone of trust; and debt recovery should be understood not as a threat, but as a necessary process to keep the wheels of our economy turning for everyone. When we honor our commitments, we not only protect our own futures, but we also invest in the growth of our businesses, the stability of our families, and the prosperity of Nigeria itself. It is time to build a credit culture that we can all rely on.

About Author:

Dr Prisca Ndu who holds four doctorate degrees in Credit Management, Banking and Finance, Leadership and Management and Artificial Intelligence, is a social impact advocate and multi-sector entrepreneur. An alumnus of the University of Ibadan, Lagos Business School, Harvard Business School, London Graduate School, Institute of Management Development, INSEAD and Robert Kennedy College, Switzerland, amongst others. She sits on the Board of several companies including INDECO, KREENO Consortium, BHLA Awards, and many more. She was listed in 2017 among the most influential people of African descent by the United Nations and is passionate about Nation Building.

What's Your Reaction?